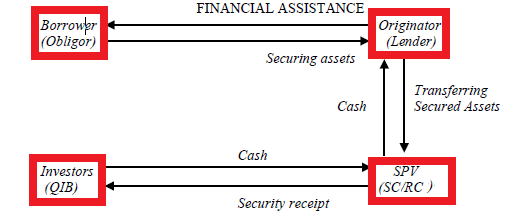

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 or SARFAESI Act, 2002 allows banks and financial institutions to auction properties (residential and commercial) when borrowers fail to repay their loans. The Act aims at speedy recovery of defaulting loans and to reduce the mounting levels of Non-performing Assets of banks and financial institutions. As stated in the Act, it has “enabled banks and FIs to realise long-term assets, manage problems of liquidity, asset-liability mismatches and improve recovery by taking possession of securities, sell them and reduce non performing assets (NPAs) by adopting measures for recovery or reconstruction.” The SARFAESI Act, 2002 has been largely perceived as facilitating asset recovery and reconstruction. The Act has been passed based on the recommendations of Narasimham Committee I and II and Andhyarujina Committee constituted by the Central Government for the purpose of examining banking sector reforms and to Continue reading

Legal Framework

The Consumer Protection Act, 1986

The consumer protection Act, 1986 is a milestone in the history of socio-economic legislation in the country. It is one of the most progressive and comprehensive pieces of legislations enacted for the protection of consumers. It was enacted after in-depth study of consumer protection laws in a number of countries and in consultation with representatives of consumers, trade and industry and extensive discussions within the Government. The main objective of the act is to provide for the better protection of consumers. Unlike existing laws, which are punitive or preventive in nature, the provisions of this Act are compensatory in nature. The act is intended to provide simple, speedy and inexpensive redressal to the consumers’ grievances, and relief’s of a specific nature and award of compensation wherever appropriate to the consumer. The act has been amended in 1993 both to extend its coverage and scope and to enhance the powers of Continue reading

An Overview of Foreign Exchange Management Act (FEMA)

The Foreign Exchange Regulation Act of 1973 (FERA) in India was repealed on 1st June, 2000. It was replaced by the Foreign Exchange Management Act (FEMA), which was passed in the winter session of Parliament in 1999. Enacted in 1973, in the backdrop of acute shortage of Foreign Exchange in the country, FERA had a controversial 27 year stint during which many bosses of the Indian Corporate world found themselves at the mercy of the Enforcement Directorate (E.D.). Any offense under FERA was a criminal offense liable to imprisonment, whereas FEMA seeks to make offenses relating to foreign exchange civil offenses. FEMA, which has replaced FERA, had become the need of the hour since FERA had become incompatible with the pro-liberalization policies of the Government of India. FEMA has brought a new management regime of Foreign Exchange consistent with the emerging frame work of the World Trade Organization (WTO). It Continue reading

The Mines Act 1952

The mines act, 1952 which was enacted to amend and consolidate the law relating to the regulation of Lob our and safety in mines came into force with effect from July 1, 1952. The act extends to whole of India and it aims at providing for safe as well as proper working conditions in mines and certain amenities to the workers employed therein. For the purpose of the act, a mines means any excavation where any operation for the purpose of searching for or obtaining minerals has been or is being carried on and includes, i) all borings, bore holes and oil wells. ii) All shafts, in or adjacent to and belonging to a mine whether in the course of being sunk or not. iii) all power stations for supply electricity solely for the purpose of working the mine or a number of mines under the same management; iv) Continue reading

The Depositories Act, 1996

The Depositories Act, 1996 was enacted to provide for regulation of depositories in securities and for matters connected therewith or incidental thereto. It came into force from 20th September, 1995. The terms used in The Depositories Act,1996 are defined as under: (1) “Beneficial owner” means a person whose name is recorded as such with a depository. (2) “Depository” means a company, formed and registered under the Companies Act, 1956 and which has been granted a certificate of registration under sub-section (1A) of section 12 of the SEBI Act, 1992. (3) “Issuer” means any person making an issue of securities. (4) “Participant” means a person registered as such under sub-section (1A) of section 12 of the SEBI Act, 1992. (5) “Registered owner” means a depository whose name is entered as such in the register of the issuer. Agreement between depository and participant A depository shall enter into an agreement in the Continue reading

Introduction to Service Tax

Service tax is a tax on service. This is not tax on profession, trade. Calling or employment but is in respect of service rendered. If there is no service, there is no tax. As per Webster’s Concise Dictionary ‘service’ means a useful result or product of labor, which is not a tangible commodity. Thus basically service is a value addition that can be perceived but cannot be seen, as it’s tangible. However, usage of some goods during the course of rendering the service would not mean that there is no ‘service’. It is the predominant factor in each case, which is to be studied to arrive at a conclusion. Service tax is a tax levied on service providers in India, except the State of Jammu and Kashmir. Service Tax, introduced from the financial year 1994-95 now covers as many as 41 services within its ambit. Service sector, which has an Continue reading