Fitzgerald and Moon’s Building Block Model suggests the solution of performance measurement problems in service industries. But it can be applied to other manufacturing and retail businesses to evaluate business performance.

Fitzgerald and Moon has provided a framework for performance management in service organization using three criteria, called as building blocks, they include, standards of performance (against these dimensions are measured to review performance), rewards for performance (rewards are necessary for achieving standards of performance) and dimensions of performance (these are measures of performance).

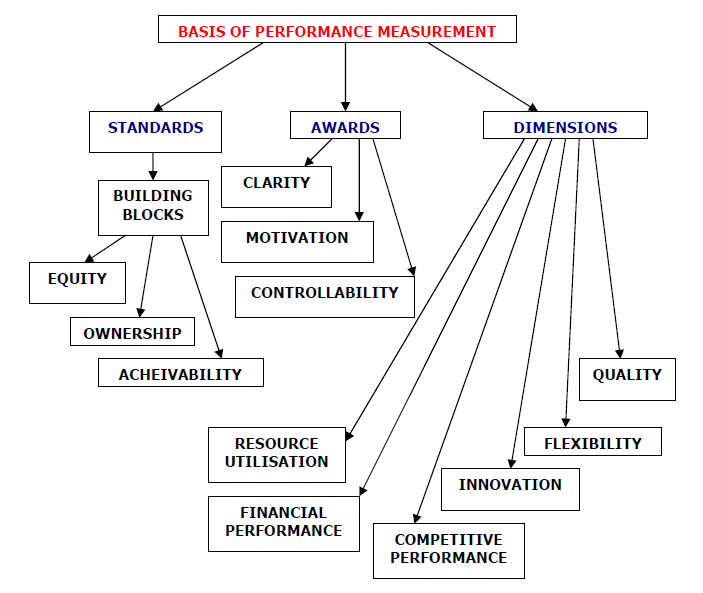

1. Standards: You can think of standards as rules that employees of a company must follow in order to achieve the long term objective of the organization. For the standards to be motivating enough, it must have three important ingredients. These ingredients are;

- Equity: Performance measures should be equally challenging for all parts of business. Relaxation given to one part of the business leads to perception of unfair treatment which hinders productivity.

- Ownership: Performance measure should be acceptable to everyone. Employees should be got involved in the identification of measures rather than being imposed on them. Ownership means here is responsibility for the results.

- Achievable: Performance measure should be realistic. Eg. Using actual results for the competitors to set as target. Employee will not be motivated to achieve targets if consider them impossible.

2. Rewards: In line with Vroom’s valence theory, managers expect to be rewarded not just for doing their job but for doing it right. To be effective, the components of rewards must be clear, concise, motivating and controllable by the employees.

- Motivation: Rewards scheme should be set in manner which motivates employees to achieve the business goals. If sales growth is desired than bonus can be linked to performance measures, like increase in number of units sold than previous year.

- Clear: Rewards scheme should be clearly communicated to employees in advance. What kind to performance will be rewarded and how their performance will be measured.

- Controllability: Employees should only be reward or penalized of the result over which they some control or influence. Aspects of business like financing and investment should not be considered by eliminating related expenses like interest and depreciation, when evaluating their performance.

3. Dimension: This basically deals with things that businesses often measure and includes, financial performance (profit), competitive performance, quality, resource utilization, flexibility and innovation. The first two elements according to the authors are directly linked to the results set by management while the last four elements of the dimension pillar relates to factors that determine or otherwise influence results.

- Financial Performance: Financial performance gives an indication of overall business at a glance in monetary terms. These can be used to identify areas of strengths and weaknesses. It may also highlight other areas previous identified which may be critical to business success.

- Competitive Performance: How they stand in comparison to its competitors? How are the different from their competitors? Eg. offering of products of higher quality than competitors and products having distinct features than rival products.

- Quality: It is the ability to deliver goods and service with consistency. Quality should be judged from eyes of the customers. Quality is the level of benefits customers expects from the product. Quality should be enough for a product price paid.

- Flexibility: It is the responsiveness to change in the factor influencing the business performance. Eg. ability to cope with sudden increase in sales demand.

- Innovation: Ability of the business to devise new products and new ways of doing things. Like packaging of products with environment friendly (recyclable) material.

- Resource Utilization: It is the ability to use resources to achieve business objectives. Business assets should be used for the proper purpose and in most efficient way. Eg. using delivery vans to its maximum capacity only by carrying authorized goods.