Legal systems and ethical codes mirror the values that people within a society have and provide the guidelines for the development of appropriate behaviors. Ethics and law continually interact with each other and affect decision making in various spheres of life. Legal duties bind employers and employees and enforce them to behave according to major ethical principles. The doctrine of vicarious liability serves as the example of this type of interactions between the law and ethics. It is the liability of the employer for the negligent acts of the employee in the course of his or her employment. Overall, it means that an employer is accountable for the wrongful or negligent torts of his/her subordinates when they are fulfilling prescribed work responsibilities and roles. Researchers and legal practitioners distinguish many ethical-legal explanations for the given rule. Some of them are analyzed in the following paragraphs. Vicarious Liability and Corporate Social Continue reading

Business Law

Ethical and Legal Justifications for The Doctrine of Vicarious Liability

Vicarious liability is a class of liabilities that deals with transfer of liability from one party to another. Vicarious liability operates under the doctrine of respondent superior, which puts legal responsibility to a superior for illegal behaviour or acts of the subordinates. Third parties are thus supposed to be ethical in their duties to avoid transfer of liability. In the same way, vicarious liability puts legal responsibilities on third parties with the duty, responsibility, or right to monitor and direct their juniors who act illegally or commit a crime. Vicarious liability can thus take the form of employers’ liability, parental liability, principals’ liability, corporations in tort liability, and continued liability, and indemnity of employees. All these liabilities have ethical issues to be considered during application. In various circumstances, it may be legal, but unethical to apply a particular vicarious liability. As aforementioned, vicarious liability operates under the doctrine of respondent superior and this doctrine Continue reading

What Is Product Liability? Meaning, Definition, and Laws

Product liability is a field of law that accounts for the responsibility of producers, manufacturers, suppliers, and other stakeholders who avail products to the general public for the injuries those products cause the public. Most of these claims are associated with negligence, breach of warranty, strict liability in addition to other forms of consumer protection claims. These laws are determined at the National level. A product liability and negligence claim justified by the product having either a manufacturer’s defect, a designing defect, or failure to warn the consumer. Generally, claims of product liability are not only based on negligence but also a strict liability. This theory of strict liability states that the manufacturer should be held liable even though the customer acted negligently. Failure to warn customers is viewed by some legal commentators as being negligent. The theory of strict liability focuses on the product of the manufacturer rather than Continue reading

SEBI (Substantial Acquisition of Shares and Takeover) Regulations Act, 1997

On the basis of recommendations of the Committee, the SEBI announced on Febuary20, 1997, the revised take over code as Securities and Exchange Board of India (Substantial Acquisitions of shares and Takeovers) Regulations, 1997. The objective of these regulations has been to provide an orderly framework within which substantial acquisitions and takeovers can take place. The salient features of this new takeover code (Regulations, 1997) may be enumerated as follows: i.Any person, who holds more than 5% shares or voting rights in any company, shall within two months of notification of these Regulation disclose his aggregate shareholding in that company, to the company which in turn, shall disclose to all the stock exchanges on which the shares of the company are listed, the aggregate number of shares held by each such person. ii.Any acquirer, who acquires shares or voting rights which (taken together with shares or voting rights, if any, Continue reading

SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to the Securities Market) Regulations, 2003

The SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to the Securities Market) Regulations, 2003 enable SEBI to investigate into cases of market manipulation and fraudulent and unfair trade practices. The regulations specifically prohibit market manipulation, misleading statements to induce sale or purchase of securities, unfair trade practices relating to securities. SEBI can conduct investigation, suo moto or upon information received by it, by an investigating officer in respect of conduct and affairs of any person dealing, buying/selling/dealing in securities. Based on the report of the investigating officer, SEBI can initiate action for suspension or cancellation of registration of an intermediary. The term “fraud” has been defined by Regulation 2(1)(c). Fraud includes any act, expression, omission or concealment committed whether in a deceitful manner or not by a person or by any other person or his agent while dealing in securities in order to induce another person with his Continue reading

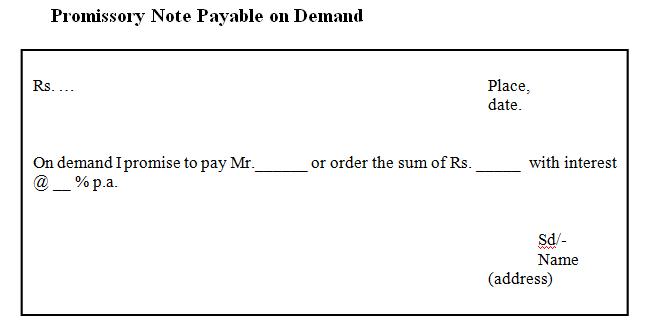

Definition and Features of Promissory Note

Promissory Note, in the law of negotiable instruments, written instrument containing an unconditional promise by a party, called the maker, who signs the instrument, to pay to another, called the payee, a definite sum of money either on demand or at a specified or ascertainable future date. The note may be made payable to the bearer, to a party named in the note, or to the order of the party named in the note. A promissory note differs from an IOU(An IOU (abbreviated from the phrase “I owe you“) is usually an informal document acknowledging debt) in that the former is a promise to pay and the latter is a mere acknowledgement of a debt. A promissory note is negotiable by endorsement if it is specifically made payable to the order of a person. According to section 4 of the Negotiable Instruments Act, 1881, a promissory note means “Promissory Note Continue reading