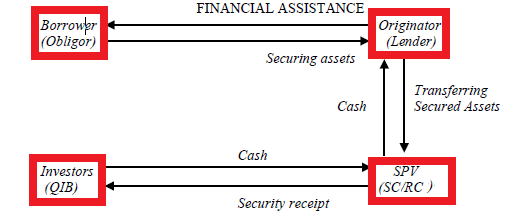

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 or SARFAESI Act, 2002 allows banks and financial institutions to auction properties (residential and commercial) when borrowers fail to repay their loans. The Act aims at speedy recovery of defaulting loans and to reduce the mounting levels of Non-performing Assets of banks and financial institutions. As stated in the Act, it has “enabled banks and FIs to realise long-term assets, manage problems of liquidity, asset-liability mismatches and improve recovery by taking possession of securities, sell them and reduce non performing assets (NPAs) by adopting measures for recovery or reconstruction.” The SARFAESI Act, 2002 has been largely perceived as facilitating asset recovery and reconstruction. The Act has been passed based on the recommendations of Narasimham Committee I and II and Andhyarujina Committee constituted by the Central Government for the purpose of examining banking sector reforms and to Continue reading

Indian Banking System

8 Risks Faced by Modern Banks at the Present Competitive Business World

The unanticipated part of the return, that portion resulting from surprises is the true risk of any investment. If we always receive what we expect, than the investment is perfectly predictable and, by definition, risk-free. In other words, the risk of owning an asset comes from surprises-unanticipated events. RISK is a concept that denotes the precise probability of specific eventualities. It is simply the future uncertainty and not only the incidents of predictable outcomes but also the unpredictable favorable outcomes. All the firms or companies whether it is in real or providing service are facing some sort of risk at present competitive business world to run its business. Banks are one of them in these regard and it is facing possibility of risk in terms of money and their achieved reputation. Bank is a financial institution that primarily deals with borrowing and lending money from the people by the people Continue reading

Lead Bank Scheme

A milestone in the history of banking in India is the nationalization of the 14 major commercial banks in 1969. This process was undertaken with the main objective of involving the banking sector in a big way in the nation building and economic development. To help to achieve this commendable objective, two committees were set up viz., National Credit Council Study Group with D.R. Gadgil as the Chairman and the Committee of Bankers under the chairmanship of Nariman. These committees independently went into their terms of reference and recommended an ‘area approach’ for involving the banks in economic development. This paved the way for giving a concrete shape to the Lead Bank Scheme. As nationalization of banks took place to extend and expand the banking services to all the non-banked areas especially the rural areas, Continue reading

Different Modes of Granting Loans by Commercial Banks

The basic function of a commercial bank is to make loans and advances out of the money which is received from the public by way of deposits.The loans are particularly granted to businessmen and members of the public against personal security, gold and silver and other movable and immovable assets. Such loans and advances are given to members of the public and to the business community at a higher rate of interest than allowed by banks on various deposit accounts. The rate of interest charged on loans and advances varies depending upon the purpose, period and the mode of repayment. The difference between the rates of interest allowed on deposits and the rate charged on the loans is the main source of a commercial banks income. A loan is granted for a specific time period. Generally, commercial banks grant short-term loans. But term loans, that is, loan for more than Continue reading

Different Modes of Acceptance of Deposits by Commercial Banks

The most important activity of a commercial bank is to mobilize deposits from the public. People who have surplus income and savings find it convenient to deposit the amounts with banks. Depending upon the nature of deposits, funds deposited with bank also earn interest. Thus, deposits with the bank grow along with the interest earned. If the rate of interest is higher, public are motivated to deposit more funds with the bank. There is also safety of funds deposited with the bank. The following types of deposits are usually received by banks: Current Deposit: Also called ‘demand deposit’, current deposit can be withdrawn by the depositor at any time by cheques. Businessmen generally open current accounts with banks. Current accounts do not carry any interest as the amount deposited in these accounts is repayable on demand without any restriction. The Reserve bank of India prohibits payment of interest on current Continue reading

Functions of Commercial Banks

The main functions of commercial banks are accepting deposits from the public and advancing them loans. However, besides these functions there are many other functions which these banks perform. Paul Samuelson has defined the functions of the Commercial bank in the following words: “The Primary economic function of a commercial bank is to receive demand deposits and a honor cheques drawn upon them. A second important function is to lend money to local merchants farmers and industrialists.” The major functions performed by the commercial banks are: 1. Accepting Deposits This is one of the primary functions of commercial banks. The commercial banks accept different types of deposits, the deposits may be broadly classified as demand deposits and time deposits. The former refer to the deposits which are repayable by the banks on demand by the depositors, while the time deposits are accepted by the banks for a fixed Continue reading