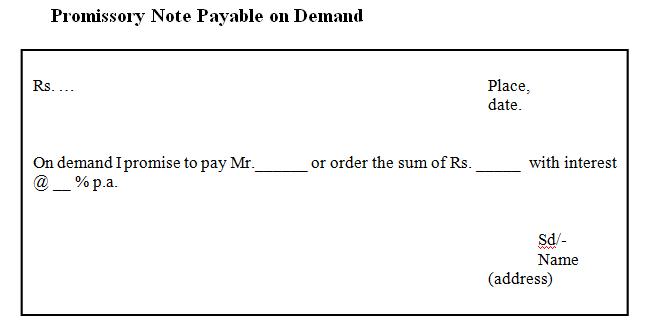

Promissory Note, in the law of negotiable instruments, written instrument containing an unconditional promise by a party, called the maker, who signs the instrument, to pay to another, called the payee, a definite sum of money either on demand or at a specified or ascertainable future date. The note may be made payable to the bearer, to a party named in the note, or to the order of the party named in the note. A promissory note differs from an IOU(An IOU (abbreviated from the phrase “I owe you“) is usually an informal document acknowledging debt) in that the former is a promise to pay and the latter is a mere acknowledgement of a debt. A promissory note is negotiable by endorsement if it is specifically made payable to the order of a person. According to section 4 of the Negotiable Instruments Act, 1881, a promissory note means “Promissory Note Continue reading

Mercantile Law

Memorandum of Association of a Company

The Memorandum of Association is the charter of the company, and provides the foundation on which the structure of the company is built. It defines the scope of the company’s activities as well as its relation with the outside world. Section 2(28)of the Companies Act defines a Memorandum as “the memorandum of association of a company as originally framed or as altered from time to time in pursuance of any previous Company Laws or of this Act”. Section 13 of the Act specifies the contents of the memorandum. The importance of the Memorandum is that it lays down the ambit of the powers of the company, the area within which the company can operate and beyond which it cannot go. The purpose of the Memorandum is to enable the shareholders, creditors and those who deal with the company to know what is its permitted range of enterprise. The Memorandum of Continue reading

Cheque: Definition, Features and its Types

Cheque is a very common form of negotiable instrument. If you have a savings bank account or current account in a bank, you can issue a cheque in your own name or in favor of others, thereby directing the bank to pay the specified amount to the person named in the cheque. Therefore, a cheque may be regarded as a bill of exchange; the only difference is that the bank is always the drawee in case of a cheque. The Negotiable Instruments Act, 1881 defines a cheque as a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand. From the above dentition it appears that a cheque is an instrument in writing, containing an unconditional order, signed by the maker, directing a specified banker to pay, on demand, a certain sum of money only to, to the order of, a certain Continue reading

Doctrine of Ultra Vires

‘Ultra’ means beyond and ‘vires’ means powers. The term ultra vires a company means that the doing of the act is beyond the legal power and authority of the company. The doctrine of ultra vires is important in defining the limits of the powers conferred on the company by its Memorandum of Association. According to this doctrine, the vires (power) of a company to enter into a contract or transaction is limited by the ambit of the Objects Clause of the Memorandum and the provisions of the Companies Act. Whatever is not permitted by the Objects Clause and the Act, is prohibited by the doctrine of ultra vires. If a company engages in any activity or enters into any contract which is ultra vires (outside the power conferred by) the Memorandum or Act, it will be null and void so far as the company is concerned and it cannot be Continue reading

Directors of a Company

A company, though a legal entity in the eyes of the law, is an artificial person, existing only in contemplation of law. It has no physical existence. It has neither soul nor a body of its own. As such, it cannot act in its own person. It can do so only through some human agency. The persons who are in charge of the management of the affairs of a company are termed as directors. They are collectively known as Board of Directors. The Companies Act defines a ‘director’ as “any person occupying the position of a director by whatever name called” [Sec.2(13)]. This is however, an inadequate definition. In the absence of a precise definition, we can only determine whether a person is a director or not a director by referring to the nature of his office and functions. According to the functions performed by him, a director may be Continue reading

Strategies Adopted in Proxy Battles

To win over proxy wars (in the case of takeover bids), where the corporate board or equity holders meetings are exposed to proxy wars, the directors have to adopt strategies based on the steps given below: Collection of material information Construction of proxy fight team Mass contact with shareholders Board of Directors of a company while facing a takeover bid have to work hard to defeat such a bid. Therefore they should collect all possible information about the affairs of their own company, competitors, the takeover — bidder and the opponents. Particularly the management of a company with small holdings on their board face stiff problem. In that case the only remedy is to allow board members to increase shareholdings. To face the opponents, the board must use all the material information available for their defense. The proxy fight team includes experts and persons of experience to help the management Continue reading