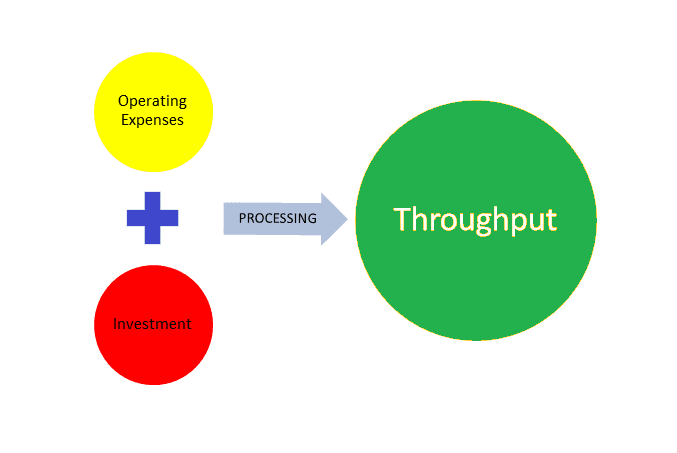

Goldratt’s ‘Throughput Accounting’ revolutionized the methods by which companies viewed their costs and associated them with profits. Unlike the traditional cost accounting methods, Goldratt argues that accounting should seek to maximize the movement of products through an organization to eliminate potential bottlenecks that prevents efficiency and speed. Goldratt argues that the current costing systems in use were developed almost a hundred years ago based upon the business practices and business designs of that particular era. The traditional accounting system therefore can be understood in the context of a “Cost World”. This cost world focuses all aspects of business value and decision making upon the cost of products themselves. In order to connect all of the subsequent aspects of business to costs, very elaborate allocation of expenses had to flow through to products. These “cost schemes” in effect have many different errors and assumptions that impacts the accuracy of accounts and Continue reading

Financial Management

Financial management entails planning for the future of a person or a business enterprise to ensure a positive cash flow, including the administration and maintenance of financial assets. The primary concern of financial management is the assessment rather than the techniques of financial quantification. Some experts refer to financial management as the science of money management. The five basic components of the Financial Management Framework are: Planning and Analysis, Asset and Liability Management, Reporting, Transaction Processing and Control.

Real Options in Capital Budgeting

Real options refer to a relatively new financial analytical tool that helps investors and managers to select market valuations that reflect a blend of businesses that are already known together with the value of business opportunities that are likely to arise. The Black-Scholes model is one of the best known forms of financial option theory that is applied through real options. There is need for managers and investors to understand how to take advantage of rapid changes that are occurring in economic world. This need if fulfilled by real options which gives them requisite insights into strategic investments and businesses. Real options are viable where particular conditions are met. Managers who are keen on maintaining the status quo will certainly miss the opportunities availed by this analytical tool. Economic changes occurring from time to time are a fertile breeding ground for real options. Businesses with adequate capital, reputable and intelligent Continue reading

Depreciation – Definition, Methods, and Tax Implications

Depreciation is a cost estimation method for accounting for the worth of a long-term asset over its useful life. Depreciation is used to spread the cost of a tangible asset over the accounting periods in which the asset is used. There are some questions surrounding this topic that are essential to explore. For instance, what are the tax implications of depreciation? What are the different depreciation methods, and how can they be used to calculate the amount? What are the best practices for managing depreciation? How does depreciation help to ensure a company’s financial health? Each of these questions will be explored in more detail to understand the concept of depreciation fully. Since antiquity, depreciation has been utilized for cost apportionment. Initially, the idea was developed by the Greek philosopher Aristotle, who believed that the value of an asset declined over time. By the 19th century, Italian economist Vilfredo Pareto Continue reading

Corporate Investment Decisions – Meaning and Stages

In order to succeed in a competitive market, corporations need to pay much attention to their investment decisions to gain benefits and profits. The process of making effective decisions involves several steps, and it needs to be discussed in detail along with a list of options that are available to corporations for their investment. The purpose of this article is to provide an explanation of how the majority of corporations make specific investment decisions to add to their profitability and competitive advantage. The first step in the decision-making process related to investing in the analysis of a current situation with the help of certain tools, such as the cash flow analysis and the analysis of the cost of capital. These tools are important to indicate the current position of a corporation in the market, evaluate its attractiveness to potential investors, and influence its own investing decisions. The second step in Continue reading

Accounting Methods Used in Financial Statement Preparation

First of all, what is the primary objective of financial statement? Financial statement is to provide information about financial position, performance and changes in financial position of an enterprise that is useful to a wide range of users in making economic decisions – stated by International Accounting Standards Board (IASB). For providing information of financial statement, there are two accounting methods for companies to report their financial statement. Cash accounting and accrual accounting both are the main method to prepare the financial statement. Cash basis accounting is a very basic form of accounting. Revenue is recorded only when the cash is received, and an expense is recorded only when cash is paid. Preparing an income statement under the cash basis of accounting is prohibited under generally accepted accounting principles. For example, when a payment is received for the sales of product or services and the revenue is also recorded the Continue reading

Bank Decisions on Investment Borrowings

Assessment of the liquidity gap based on the forecasts is essentially one aspect of the liquidity management. The other major task of liquidity management is to manage this liquidity gap by adjusting the residual surplus/deficit balances. Considering the high costs associated with cash forecasting, it is essential that the benefits drawn by the bank from such forecasting should be substantially large to give some residual gains after meeting the forecasting costs. This objective can, however, be attained only if the bank makes prudent investment/borrowing decisions to manage the surplus/deficit. There are, however, a few factors which must be considered before deciding on the deployment of excess funds/borrowings for meeting the deficit which are given below: Deposit Withdrawals Credit Accommodation Profit fluctuation The liquidity level to be maintained by a bank should firstly, provide for deposits withdrawals and secondly to accommodate the increase in credit demands. While deposit withdrawals must be Continue reading