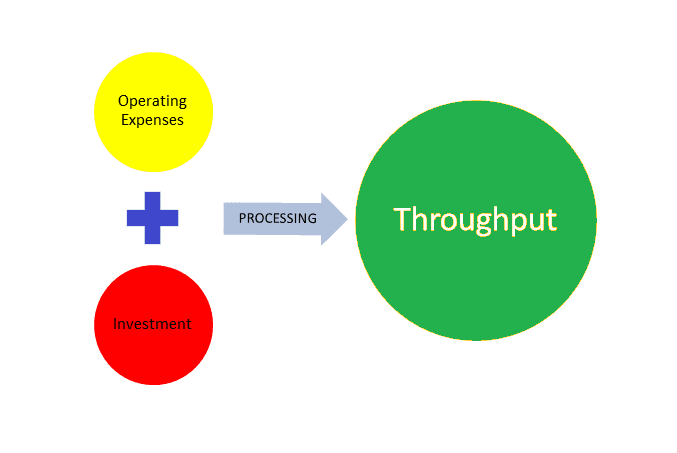

Goldratt’s ‘Throughput Accounting’ revolutionized the methods by which companies viewed their costs and associated them with profits. Unlike the traditional cost accounting methods, Goldratt argues that accounting should seek to maximize the movement of products through an organization to eliminate potential bottlenecks that prevents efficiency and speed. Goldratt argues that the current costing systems in use were developed almost a hundred years ago based upon the business practices and business designs of that particular era. The traditional accounting system therefore can be understood in the context of a “Cost World”. This cost world focuses all aspects of business value and decision making upon the cost of products themselves. In order to connect all of the subsequent aspects of business to costs, very elaborate allocation of expenses had to flow through to products. These “cost schemes” in effect have many different errors and assumptions that impacts the accuracy of accounts and Continue reading

Financial Management Tools

Real Options in Capital Budgeting

Real options refer to a relatively new financial analytical tool that helps investors and managers to select market valuations that reflect a blend of businesses that are already known together with the value of business opportunities that are likely to arise. The Black-Scholes model is one of the best known forms of financial option theory that is applied through real options. There is need for managers and investors to understand how to take advantage of rapid changes that are occurring in economic world. This need if fulfilled by real options which gives them requisite insights into strategic investments and businesses. Real options are viable where particular conditions are met. Managers who are keen on maintaining the status quo will certainly miss the opportunities availed by this analytical tool. Economic changes occurring from time to time are a fertile breeding ground for real options. Businesses with adequate capital, reputable and intelligent Continue reading

Role of Financial Statements Analysis in Making Investment Decisions

One of the most important long-term decisions for any business is investment with the aim of making gains in the future. Investment decisions are concerned with the use of funds including buying, holding or selling and each decision could be vital to a firm. A careless decision may result in a long-term loss or even worse, bankruptcy. Therefore, an in-depth understanding and analysis is necessary for a high quality investment decision process. This is also even more critical to investors who invest in stock of company or shareholders. Financial statement analysis is critical in making effective stock investment decisions. By study the balance sheet, income statement, cash flow statement and statement of owners’ equity separately and combined, an analyst might have a good sense of a company’s overall financial picture; therefore, the investment decisions are likely to be reasonable and profitable. Financial Statements Analysis In order to understand the analysis Continue reading

Fama and French Three Factor Model

Capital Asset Pricing Model (CAPM) is the backbone of modern portfolio theory. According to CAPM, the expected return on stock is a function of its relationship with the market portfolio defined by its beta. However, Eugene Fama and Kenneth French (1992) brought together two more factors and found that stock return is based on a combination of not just market beta but also firm size and value. They came up with a new model known as Three Factor Model as an alternative to CAPM. What is Fama and French Three Factor Model? Fama and French three factor model expands on the Capital Asset Pricing Model (CAPM) by adding size and value factors in addition to the market risk factor in CAPM. This model considers the fact that value and small cap stocks out-perform markets on a regular basis. Fama and French attempted to approach and measure equity returns in a Continue reading

Benefits of Securitization

Securitization, also known as asset-backed securitization or structured financing, has been defined as a financing instrument whereby a company transfers rights in current or future receivables or other financial assets to an entity that serves as a “special purpose vehicle” (SPV), which in turn issues securities to capital market investors and uses the proceeds from the issue to pay for the financial assets. The source of the receivables could be any right of payment or asset that generates an income with a stable cash flow. The existing or future receivables could be the income generated, among others things by residential or commercial loans, credit card receivables, automobile loans, student loans, royalties on intellectual property, tax receivables or any other income source that is regular and predictable. Read More: The Concept of Securitization Securitization can also be considered a form of arbitrage between a less-efficient traditional debt market and a more-efficient Continue reading

What is Return on Investment (ROI)?

Return on Investment (ROI) refers to a well-known financial metric commonly used to analyze the financial results which arise from personal investments as well as deeds. A number of varying metrics are basically known by the same definition. Normally used as a cash flow metric, the Return on Investment particularly makes a comparison of the scale as well as scheduling of investment gains which are matched directly to the scale and scheduling of costs involved. In any situation where the ROI is seen to post a high rate, it implies that the gains which have been made compare well with the costs that had been incurred. Return on Investment (ROI) = (Net Profit or Gain / Cost of Investment) * 100 Return on Investment has grown into a well-known concept within the past few decades mostly as an all-purpose metric for analyzing capital attainments, business initiatives, and conservative fiscal investments. These Continue reading