Whether the movement of material and equipment is by rail, sea, air or road, adequate facilities for their free flow to and from the factory must be ensured. The factors which affect progress at the construction stage, and production and dispatches after commission, have been discussed below: 1. Terminal Facilities Terminal facilities are usually grudgingly provided. One reason for this is that any delay or any in convenience caused to truck operators is not a loss to the project. It is treated as a loss to the carrier. In some cases, this may be true. However, this usual incidence of stoppage or regulation of the production process can be minimized, if not eliminated. Often extreme stinginess is expressed in planning for these facilities, which include storage space, and loading and unloading arrangements in a suitable area. If the storage space is not adequate or if the traffic is exceptionally heavy, Continue reading

Logistics Basics

Concept of Strategic Logistics Planning

Strategic logistics planning is defined as a unified, comprehensive, and integrated planning process to achieve competitive advantage through increased value and customer service, which results in superior customer satisfaction, by anticipating future demand for logistics services and managing the resources of the entire supply chain. Strategic logistics planning carried out within the framework of the overall corporate goals and plan. It therefore requires an in-depth understanding as to how the different elements and logistics activities relate in terms of trade-offs and the total cost to the organisation. Logistics can therefore best formulate its own strategy only by understanding the overall corporate strategy. Formulating the Strategic Logistics Plan The development of the strategic logistics plan is dependent on the marketing, manufacturing, finance/accounting and logistics functional areas. Marketing provides information about product or service offerings, pricing and promotion for each channel. This includes planned sales volume per month, type of customer, and Continue reading

Concept of Shipping Conferences in Logistics

The conferences are association of companies, resembling an ordinary cartel or trust, formed to control supply and prices and to limit entry into the trade. The Royal Commission of 1909 defined Shipping ring or conference as ‘a combination, more or less close of shipping companies formed for the purpose of regulating or restricting competition in the carrying trade on a given trade route or routes’. Shipping Conferences are formed only in a line trade and not in the tramp service, because the former is a more stable and regular organisation. Since the conferences are made for particular routes only, a shipping company may join many conferences on different routes. Likewise, the shipping companies may not join conference of a particular route and carry on independent business. The organisation of conferences varies. It may be completely formal or informal. A conference may have liners of various nationalities as its members and Continue reading

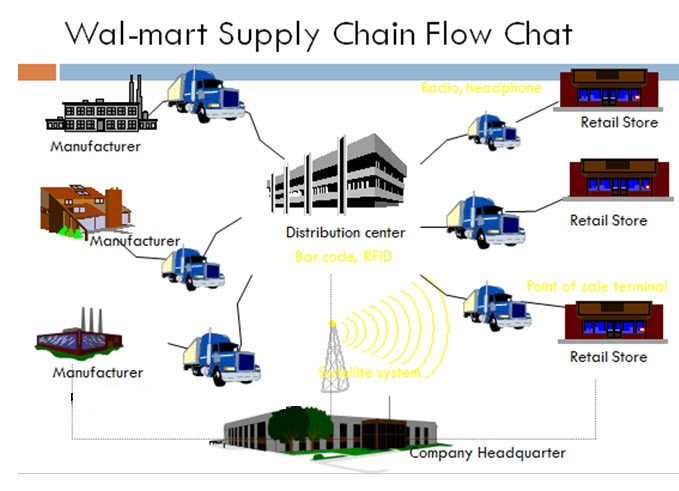

Case Study: Wal-Mart’s Distribution and Logistics System

As the world’s largest retailer with net sales of almost $419 billion for the fiscal year 2011, Wal-Mart is considered a “best-in-class” company for its supply chain management practices. These practices are a key competitive advantage that have enabled Wal-Mart to achieve leadership in the retail industry through a focus on increasing operational efficiency and on customer needs. Wal-Mart’s corporate website calls “logistics” and “distribution” the heart of its operation, one that keeps millions of products moving to customers every day of the year. Wal-Mart’s highly-automated distribution centers, which operate 24 hours a day and are served by Wal-Mart’s truck fleet, are the foundation of its growth strategy and supply network. In the United States alone, the company has more than 40 regional distribution centers for import flow and more than 140 distribution centers for domestic flow. When entering a new geographic arena, the company first determines if the Continue reading

Effective Logistics and Competitive Advantage

Effective logistics management can provide a major source of competitive advantage. The bases for successes in the marketplace are numerous, but a simple model has been based around the three C’s — Customer, Company & Competitor. The source of competitive advantage is found firstly in the ability of the organization to differentiate itself, in the eyes of the customer, from its competition and secondly by operating at a lower cost and hence at greater profit. Seeking a sustainable competitive advantage has become the concern of every manager who realizes the realities of the marketplace. It is no longer acceptable to assume that the goods will sell themselves. An elemental, commercial success is derived either form a cost advantage or a value advantage or, ideally both. The greater the profitability of the company the lesser is the cost of production. Also a value advantage gives the product an advantage over the Continue reading

Warehousing Function of Logistics

A warehouse is a location with adequate facilities where volume shipments are received from a production center, broken down, resembled into combinations representing a particular order or orders and shipped to the customer’s location or locations. The rationale for establishing a warehouse in a distribution network is the creation of a differential advantage for the firm. This advantage accrues from achieving a lower overall distribution cost and/or obtaining service advantage in a market area. The concept of a distribution warehouse or a distribution center is vastly different from the earlier concept of a godown for storage. The need of that system is sue to Ensuring protection against delays and uncertainties in transportation arising from a variety of factors. Eliminating lack of sophistication in production control and consequent uncertainties in the availability of product at the desired time and place. Providing for adjustment between the time of production and the time Continue reading