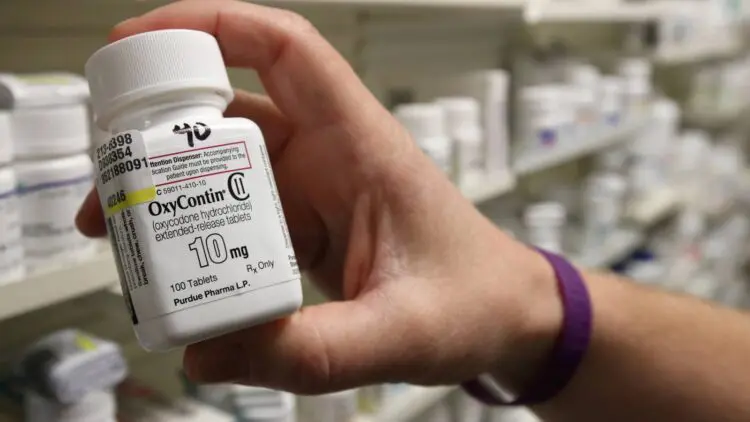

McKinsey and Company, a leading consulting agency, has agreed to pay US$573 as a settlement for advising Purdue Pharma, a drug company, on how to “supercharge” opioid sales. The agreement to pay the settlement was reached after the management of the consultation firm agreed with attorney generals of 47 states, Massachusetts court records revealed. This action disrespects human rights, especially for the patients of the drug produced by Purdue Pharma. The decision to settle was made in February 2021 when the Company’s unethical advice to the pharmaceutical organization was disclosed. For about a decade, McKinsey advised Purdue on ways to brand and market opioids and influence doctors into prescribing high doses of opioids. The consulting firm also ensured that Purdue maximized its profits by offering guidance on evading pharmaceutical prescriptions. In addition, McKinsey was also known to be involved with other opioid-related works, including consulting advice to Johnson & Johnson, Continue reading

Business Ethics

Business ethics (also known as corporate ethics) is a form of applied ethics or professional ethics that examines ethical principles and moral or ethical problems that arise in a business environment. It applies to all aspects of business conduct and is relevant to the conduct of individuals and business organizations as a whole. Business ethics can be both a normative and a descriptive discipline. As a corporate practice and a career specialization, the field is primarily normative. In academia descriptive approaches are also taken. The range and quantity of business ethical issues reflects the degree to which business is perceived to be at odds with non-economic social values.

Case Study on Business Ethics: The Wells Fargo Fake Accounts Scandal

Wells Fargo, one of the largest and most profitable banks in America, struggles to repair its dented image after it was caught in a mega fraudulent accounts scandal. The San Francisco-based bank had its management pressure on its employees to meet unrealistic sales targets, which led to the fake account incident. The customers were forced to pay bank charges they did not know about, and it was much later that the scandal was unraveled. Between 2011 and 2015, more than 1.5 million accounts were opened by Wells Fargo employees, and 565,000 credit cards were applied in customer’s names without their authorization. During a lawsuit by the government regulatory bodies, the Securities and Exchange Commission (SEC), the Department of Justice (DOJ), and the Federal Reserve, it was established that Wells Fargo blatantly falsified its bank records. Apart from the hefty fines that have been imposed on Wells Fargo, there are lessons Continue reading

Earnings Management – Definitions, Reasons and Examples

Earnings Management (EM) is the term used to describe the process of manipulating earnings of the firm to meet management’s predetermined target. The flexibility of accounting standards may cause some variability in earnings to occur as a result of the accounting choices made by management. However, earnings management that falls outside the generally accepted accounting choice boundaries is clearly unethical. The intent behind the earnings management also contributes to the questionable ethics of the practice. Some managers use EM as a means of deceiving shareholders or other stakeholders of the organization, such as creating the appearance of higher earnings to increase compensation or to avoid default on a debt covenant. The intent to use EM to deceive stakeholders implies that it can be unethical, even if the earnings management remains within the boundaries of GAAP or IAS. Earnings management has been defined as management’s exploitation of accounting flexibility to meet Continue reading

Case Study on Corporate Governance: WorldCom Scandal

Established in 1988, WorldCom was formed so that the strongest, most capable public relations firms could serve national and international clients, while retaining flexibility and client- service focus inherent in independent agencies. Through WorldCom, clients have on demand access to in-depth communication expertise from professionals who understand the language, culture and customs in the geographic areas of operation. WorldCom has 105 offices in 90 cities and 40 countries on five continents, more than 2000 employees and recorded revenue of US $ 243.5 million in 2008. In the 90’s WorldCom was involved in acquisitions and purchased over 60 firms. The complete financial integration of the acquired company must be accomplished, including an accounting of assets, debts, and a host of other financially important factors. WorldCom moved into Internet Traffic, controlling 50% of US Internet Traffic and 50% of the e-mails worldwide. In 1997, WorldCom and MCI completed a US $37 billion Continue reading

Audit Committee – Meaning, History, Roles, and Responsibilities

Corporate governance plays an important role in disciplining the management of the company like transparency in financial reporting and having robust internal controls. Enormous responsibilities like audit committee, duty of the auditors and induction of non-executive directors to act independently have been inflicted on the management of the company and any deviations will be viewed seriously and action against directors can be initiated by the compliance authorities. Audit committee, which is a group of directors who are not concerned with day-today management of the company but supervising how business is administered, conducted and reported. A committee of directors which is entrusted with the precise duty to evaluate the yearly financial reports of the business is known as the audit committee. An audit committee acts as a link between the board of directors and the auditor which includes the evaluation of the statutory audit report, the suggestion of the auditors, the Continue reading

Consumerism – Meaning and Effects

Consumerism refers to the process by which individuals acquire new goods and services without making some important considerations. Some of these considerations that the consumers do not mind are their need for the product and the durability of the product. They also do not mind the effects of the manufacture and disposal of the product to the environment. Companies spend huge sums of money to advertise their products so as to create a desire for the product by the consumers. The advertisements convince the consumers that the products are very important and that it is very beneficial for them to acquire the products. Those who acquire the products are convinced that they have made an achievement. Consumerism leads to materialism where consumers are preoccupied with the acquisition of material objects, comforts and considerations and have no concern on the spiritual, intellectual, and cultural values. Consumerism has many effects on the Continue reading