Project advisory services falls under one of the core branches of corporate advisory services. It deals with the decision of financing a project based on its strength of assuring the future cash inflows. In other words Project financing deals with financing a project, which can in turn generate return for its stakeholders and help in repaying the interest and loan on the proposed project. The assets used for undertaking that project are used as collateral for financing that project. The following constitute the differences between project financing and the other types. In project financing, the lenders look at the strength of the project to perform and generate sufficient returns to serve the interest and loan on that project. Even if the assets are taken as collateral, they may not be able to cover the entire loan through the sale of assets. Hence the lenders mainly look about the profitability of Continue reading

Business Finance

Business Finance is that business activity which is concerned with the acquisition and conservation of capital funds in meeting financial needs and overall objectives of business enterprises.

Flexible Budgets – Definition, Characteristics and Preparation Methods

Meaning of Flexible Budgeting Defining the term budgeting is helpful in understanding its role in an entity. Budgeting is described as a quantitative reflection of a business or an individual plan on the use of resources for a specified period of time, in many instances per year. In simpler terms, budgeting is the generation of a document that brings together approximations of income and expenditure for an upcoming period. Given the small duration that is covered, budgeting is also viewed as short-term financial arrangement or plan. In addition, budgets are taken as representations of action plans that help managers pursue business objectives. Thus, it is summed that budgeting is a comprehensive and coordinated plan, based on financial figures, pertaining to operations and resources used in an organization for a specified duration in the future. The overall objective of the budgetary process is to improve the performance of the organization. Comprehending Continue reading

Functions of Commercial Banks

The main functions of commercial banks are accepting deposits from the public and advancing them loans. However, besides these functions there are many other functions which these banks perform. Paul Samuelson has defined the functions of the Commercial bank in the following words: “The Primary economic function of a commercial bank is to receive demand deposits and a honor cheques drawn upon them. A second important function is to lend money to local merchants farmers and industrialists.” The major functions performed by the commercial banks are: 1. Accepting Deposits This is one of the primary functions of commercial banks. The commercial banks accept different types of deposits, the deposits may be broadly classified as demand deposits and time deposits. The former refer to the deposits which are repayable by the banks on demand by the depositors, while the time deposits are accepted by the banks for a fixed Continue reading

Risk Management in Banks: Regulatory Issues and Capital Adequacy

Individual banks risks create Systematic risk, i.e., the risk that the whole banking system fails. Systematic risk results from the high interrelations between banks through mutual lending and borrowing commitments. The failure of single institution generates a risk of failure for all banks that have ongoing commitments with the defaulting bank. Systematic Risk is a major challenge for the regulator. A number of rules, aimed at limiting risks in a simple manner, have been in force for a long time. For instance, certain ratios are subject to minimum values, say Capital Adequacy Ratio, certain caps are placed viz., Single Borrowers etc., so as to limit the risks. The main enforcement of such regulations is Capital Adequacy. That is by enforcing a capital level in a level in a line with risks, regulators focus on pre-emptive (in-anticipation) actions limiting the risk of failure. Guidelines are defined by a group of regulators Continue reading

By-Product – Meaning and Accounting Treatment

Salable or usable products having a relatively low value incidentally realized in the course of manufacturing the main product is called by-product. In many instances, there may be several joint products and several by-products depending upon the nature of the input raw materials being processed. A by-product is an outcome that does not make tangible contribution to the sales revenue. The economic value of by-product, comparing it with the main product, is comparatively low. By-product in the course of sugar production are Bagasse of solid waste and molasses of sweet semi-liquid product. Poultry farm in delivering chicken meat to the market gets poultry leftover parts such as poultry fathers, bones, beaks, feet and poultry fat as by-product. The fibers and outer shell of coconut are the by-products residue of coconut oil and product. Accounting Treatment of By-Product By-product accounting depends on the circumstances under which it is realized. The following could be Continue reading

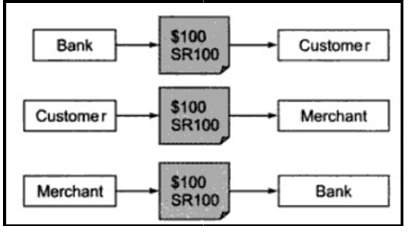

An Overview of Electronic Cash

The World is moving rapidly with vastly changing technological developments and innovations. We are currently experiencing an era, where everything is getting automated and digitalized. Along with this technological transition, international monetary system is one significant aspect that is getting transferred from its current state of paper based monetary system to electronic monetary/cash system. According to the 1994 report of European Central bank, electronic cash can be defined as an electronic store of monetary value on a technical device that may be widely used for making payments to undertakings other than the issuer without necessarily involving bank accounts in the transaction, but acting as a prepaid bearer instrument. Like the serial number on general dollar bills, electronic cash issued by a bank or any other institution will also consist a unique number and will represent a specified value of real money. Hence with the current accelerated phase of changes and Continue reading