Merger is a financial tool that is used for enhancing long-term profitability by expanding their operations. Mergers occur when the merging companies have their mutual consent. The income tax Act, 1961 of India uses the term ‘amalgamation’ for merger. The procedure of amalgamation or merger is long drawn and involves some important legal dimensions. Following Steps are Taken in this Procedure Analysis of proposal by the companies: whenever a proposal for merger or amalgamation comes up then managements of concerned companies look into the pros and cons of the scheme. The likely benefits such as economies of scale, operational economies, improvement in efficiency, reduction in cost, benefits of diversification, etc. are clearly evaluated. The likely reaction of shareholders, creditors and others are also assessed. The taxation implications are also studied. After going through the whole analyses work, it is seen whether the scheme will be beneficial or not. After going Continue reading

Legal Framework

Micro, Small and Medium Enterprises Development Act, 2006

An Act to provide for facilitating the promotion and development and enhancing the competitiveness of micro, small and medium enterprises and for matters connected therewith or incidental thereto. Whereas a declaration as to expediency of control of certain industries by the Union was made under section 2 of the Industries (Development and Regulation) Act, 1951; And whereas it is expedient to provide for facilitating the promotion and development and enhancing the competitiveness of micro, small and medium enterprises and for matters connected therewith or incidental thereto; Be it enacted by Parliament in the Fifty-seventh Year of the Republic of India as follows: 1. Short title and commencement. (1) This Act may be called the Micro, Small and Medium Enterprises Development Act, 2006. (2) It shall come into force on such date as the Central Government may, by notification, appoint; and different dates may be appointed for different provisions of this Continue reading

The Payment of Bonus Act, 1965

The practice of paying bonus in India appears to have originated during First World War when certain textile mills granted 10% of wages as war bonus to their workers in 1917. In certain cases of industrial disputes demand for payment of bonus was also included. In 1950, the Full Bench of the Labour Appellate evolved a formula for determination of bonus. A plea was made to raise that formula in 1959. At the second and third meetings of the Eighteenth Session of Standing Labour Committee (G. O.I.) held in New Delhi in March/April 1960, it was agreed that a Commission be appointed to go into the question of bonus and evolve suitable norms. A Tripartite Commission was set up by the Government of India to consider in a comprehensive manner, the question of payment of bonus based on profits to employees employed in establishments and Continue reading

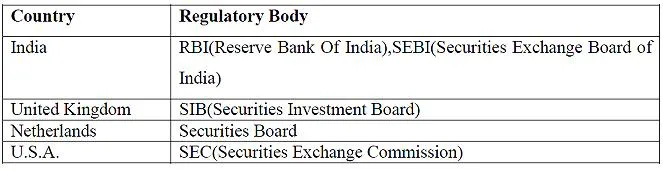

Financial Market Regulation: Meaning and Objectives

Financial Market Regulation The nature of securities markets is such that they are inherently susceptible to failures due to the existence of information asymmetries and existence of high transaction costs. It needs to be emphasized that when securities markets come into existence, the interest of the member brokers are taken care of through margin requirements, barriers to entry of membership, listing agreements. However the investors/clients who buy and sell via their brokers are not able to form an organization to safeguard their interests due to the cost of creation of such organizations and free rider problems. The distinctive nature of the market can be observed with reference to the commodity, its quality, the system of transactions and the participants in the market, as follows: (a) the commodity(the security)has a life to perpetuity. (b) while the outcome of the contract say the redemption of debt is certain, in the case of Continue reading

The Minimum Wages Act, 1948

Introduction: Wages means all remuneration capable of being expressed in terms of money, which Would, if the terms of contract of employment, express or implied, were fulfilled, be payable to a person employed in respect of his employment or of work done in such. Employment it includes house rent allowance but does not include the value of any house accommodation, supply or light, water, medical attendance or other amenity or service excluded by general or special order of appropriate Government; contribution paid by the employer to Pension/ Provident Fund or under scheme of social insurance; traveling allowance or value of traveling concession; sum paid to the person employed to defray special expenses entailed on him by the nature of his employment; or any gratuity payable on discharge. As of now there is no uniform and comprehensive wage policy for all sectors of the economy in India. Wages in the organized Continue reading

Legal and Regulatory Framework for Mutual Funds in India

Securities and Exchange Board of India (SEBI) is the apex regulator of Indian capital markets. Issuance and trading of capital market instruments and regulation of capital market the intermediaries is under the purview of SEBI. SEBI is the primary regulator of mutual funds in India. SEBI has enacted the SEBI (Mutual Funds) Regulations, 1996, which provides the scope of the regulation of mutual funds in India. It is mandatory that mutual funds should be registered with SEBI. The structure and the formation of mutual funds, appointment of key functionaries and investors, investment restrictions, compliance and penalties are all defined under SEBI Regulations, Mutual funds have to send a seven-year compliance reports to SEBI. SEBI is also empowered to periodically inspect mutual fund organizations to ensure compliance with SEBI regulations. SEBI also regulates other fund constituents such as AMCs, Trustees, Custodians, etc. Reserve Bank of India capital adequacy(RBI) is the monetary Continue reading