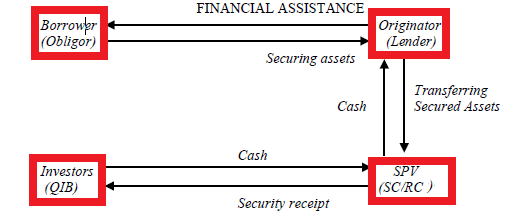

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 or SARFAESI Act, 2002 allows banks and financial institutions to auction properties (residential and commercial) when borrowers fail to repay their loans. The Act aims at speedy recovery of defaulting loans and to reduce the mounting levels of Non-performing Assets of banks and financial institutions. As stated in the Act, it has “enabled banks and FIs to realise long-term assets, manage problems of liquidity, asset-liability mismatches and improve recovery by taking possession of securities, sell them and reduce non performing assets (NPAs) by adopting measures for recovery or reconstruction.” The SARFAESI Act, 2002 has been largely perceived as facilitating asset recovery and reconstruction. The Act has been passed based on the recommendations of Narasimham Committee I and II and Andhyarujina Committee constituted by the Central Government for the purpose of examining banking sector reforms and to Continue reading

Indian Banking System

Operational Risks in Banks

“Operational Risk is defined as the risk of direct or indirect loss resulting from inadequate or failed internal processes, people and system or from external events.” Generally, operational risk is defined as any risk, which is not categorized as market or credit risk, or the risk of loss arising from various types of human or technical error. It is also synonymous with settlement or payments risk and business interruption, administrative and legal risks. Operational risk has some form of link between credit and market risks. An operational problem with a business transaction could trigger a credit or market risk. Indeed, so significant has operational risk become that the Bank for International Settlement (BIS) has proposed that, as of 2006, banks should be made to carry a Capital cushion against losses from this risk. Managing operational risk is becoming an important feature of sound risk management practices in modern financial markets Continue reading

Virtual Banking in India

The practice of banking has undergone a significant transformation in the nineties. While banks are striving to strengthen customer relationship and move towards ‘relationship banking’, customers are increasingly moving away from the confines of traditional branch-banking and are seeking the convenience of remote electronic banking services. And even within the broad spectrum of electronic banking, the aspect of banking that has gained currency is virtual banking. Increase in the functional and geographical spread of banks has necessitated the switchover from hard cash to paper based instruments and now to electronic instruments. Broadly speaking, virtual banking denotes the provision of banking and related services through extensive use of information technology without direct recourse to the bank by the customer. The origin of virtual banking in the developed countries can be traced back to the seventies with the installation of Automated Teller Machines (ATMs). It is possible to delineate the principal types Continue reading

Committee on Indian Banking Sector Reforms: Narasimham Committee Report I & II

The banking sector reforms in India were started as a follow up measures of the economic liberalization and financial sector reforms in the country. The banking sector being the life line of the economy was treated with utmost importance in the financial sector reforms. The reforms were aimed at to make the Indian banking industry more competitive, versatile, efficient, productive, to follow international accounting standard and to free from the government’s control. The reforms in the banking industry started in the early 1990s have been continued till now. The Narasimham Committee laid the foundation for the reformation of the Indian banking sector. Constituted in 1991, the Committee submitted two reports, in 1992 and 1998, which laid significant thrust on enhancing the efficiency and viability of the banking sector. The purpose of the Narasimham Committee I was to study all aspects relating to the structure, organization, functions and procedures of the Continue reading

Role of Financial Institutions in Economic Development

Financial institutions form the backbone of a modern economy, serving as crucial intermediaries that facilitate the flow of money and capital. By mobilizing savings, providing credit, and offering a spectrum of financial services, these institutions contribute to economic growth and development. Financial institutions provide means and mechanism of transferring resources from those who have an excess of income over expenditure to those who can make productive use of the same. The commercial banks and investment institutions mobilize savings of people and channel them into productive uses. Financial institutions provide all type of assistance required for economic development in the following ways. 1. Providing Funds The underdeveloped countries have low levels of capital formation. Due to low incomes, people are not able to save sufficient funds which are needed for sensing up new units and also for expansion, diversification and modernization of existing units. The persons who have the capability of starting Continue reading

Know Your Customer (KYC) Guidelines in Banking

Know Your Customer (KYC) It is important, in these days of drugs smuggling, terrorism, financial fraud, money laundering and arms dealing that banks know whom their customers are. Banks must be comfortable with the bona fides and the integrity of their customers. The need increases as external people like general selling agents introduce a number of customers. Apart from this, in order to develop a long- term relationship, it is an imperative that the banker knows as much as possible about his customer. What does KYC mean? It means that a banker should know his customers. He should know about their business and as far as possible the nature of their earnings and their moral standing. This is why it is recommended that persons known to the bank recommend prospective customers. Even though the introducers cannot be sued or otherwise held responsible, the introducers have a moral responsibility. A banker Continue reading