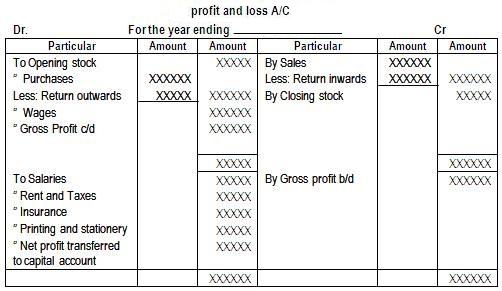

The earning capacity and potential of the firm are reflected by the Income Statement or the Profit and Loss Account. The profit and loss account is the “scoreboard” of the firm’s performance during a particular period of time (usually one year). Since it reflects the results of operations for a period of time, it is a flow statement. In contrast, the balance sheet is a stock, or status statement as it shows assets, liabilities and owners’ equity at a point of time. The profit and loss account presents the summary of revenues, expenses and net income (or net loss) of a firm for a period of time.… Read the rest

Financial Management

Financial management entails planning for the future of a person or a business enterprise to ensure a positive cash flow, including the administration and maintenance of financial assets. The primary concern of financial management is the assessment rather than the techniques of financial quantification. Some experts refer to financial management as the science of money management. The five basic components of the Financial Management Framework are: Planning and Analysis, Asset and Liability Management, Reporting, Transaction Processing and Control.

Balance Sheet

Balance sheet is one of the most significant financial statements. It indicates the financial condition or the state of affairs of a business at a particular moment of time. More specifically, balance sheet contains information about resources and obligations of a business entity and about its owners’ interests in the business at a particular point of time. Thus, the balance sheet of a firm prepared on 31st December 2011 reveals the firm’s financial position on this specific date. In accounting’s terminology, balance sheet communicates information about assets, liabilities and owner’s equity for a business firm as on a specific date. … Read the rest

Financial Accounting vs Management Accounting

Financial Accounting and Management Accounting are two interrelated facets of the accounting system. They are not exclusive of each other; they are supplementary in nature. Financial accounting provides the basic structure for collecting data. The data collection structure is suitably modified or adjusted for accumulating information for management accounting purposes.

In a broader sense, management accounting includes financial accounting. They differ in their emphasis and approaches. They are as follows:

- Financial accounting serves the interest of external users (i.e. investors etc.) while management accounting caters to the needs of internal users (i.e. management).

- Financial accounting is governed by the generally accepted accounting principles while management accounting has no set principles.

Management Accounting – Definition, Nature and Functions

That part of accounting system which facilitates the management process of decision-making is called management accounting. Basically it is the study of managerial aspect of financial accounting, “accounting in relation to management function”. It shows how the accounting function can be re-oriented so as to fit it within the framework of management activity. It presents accounting information in such a way as to assist management in the creation of policy and in the day-to-day operations of an undertaking. Management accounting has the ability to communicate a great variety of facts in a systematic and meaningful manner. The task of management accounting is not to make decisions; rather it facilitates the process of decision-making. … Read the rest

Importance of an Accounting System

Business enterprises are created for achieving one or more objectives — profit motive being the most dominant among all objectives. For accomplishing objectives efficiently and effectively, the firm needs resources which must be optimally utilized. The firm faces the question of the use and allocation of resources at two levels. First, at the macro level, the firm has to compete for resources with other firms in the capital market. The criterion used by the capital market to allocate resources is efficiency, which is conventionally measured in terms of profits. A firm would thus succeed to obtain funds from the capital market if it has been profitable in the past, or has a profit making potential in the future.… Read the rest

Inventory Management

What is inventory? What are its varieties? Inventory is the buffer between two related sequential activities. Between purchase and production, between the beginning and completion of production, and between production and marketing, buffers are needed. Buffer means a cushion to fall back on. Production should not suffer due to some difficulty in purchase of raw materials. Marketing should not suffer due to some difficulty in production. If the business has some stock of raw materials, a temporary difficulty in purchase will not effect production since the stock of raw materials can be used. If there is a stock of finished goods marketing will not be effected due to any temporary hurdle in production.… Read the rest