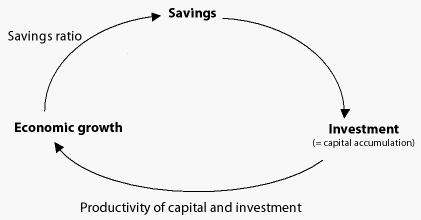

The Harrod-Domar models of economic growth are based on the experience of advanced economies. They are primarily addressed to an advanced capitalist economy and attempt to analyze the requirements of steady growth in such economy. Both Harrod and Domar are interested in discovering the rate of income growth necessary for smooth and uninterrupted working of the economy. Though their models differ in details, yet they arrive at similar conclusions. Harrod and Domar assign a key role to investment in the process of economic growth. But they lay emphasis on the dual character of investment. Fist, it creates income, and secondly, it augments the productive capacity of the economy by increasing its capital stock. The former may be regarded as the ‘demand effect’ and the later the ‘supply effect’ of investment. Hence so long as net investment is taking place, real income and output will continue to expand. However, for maintaining Continue reading

Managerial Economics

Managerial Economics generally refers to the integration of economic theory with business practice. It deals with the use of economic concepts and principles of business decision making. Managerial Economics is thus constituted of that part of economic knowledge or economic theories which is used as a tool of analyzing business problems for rational business decisions. Managerial economics can be viewed by most modern economists as a practical application of economics theory in using effectively the firms scarce resources.

Roles of Managerial Economist in Business

A managerial economist can play a very important role by assisting the management in using the increasingly specialized skills and sophisticated techniques, required to solve the difficult problems of successful decision-making and forward planning. In business concerns, the importance of the managerial economist is therefore recognized a lot today. In advanced countries, large companies employ one or more economists. A managerial economist can contribute to decision-making in business in specific terms. Different roles of managerial economist in business as follows: Environmental Studies of a Business Firm An analysis and forecast of external factors constituting general business conditions, for example, prices, national income and output, volume of trade, etc., are of great significance since they affect every business firm. Certain important relevant factors to be considered in this connection are as follows: The outlook for the national economy, the most important local, regional or worldwide economic trends, the nature of phase Continue reading

Price Discrimination in Managerial Economics

In today’s economies where product and service competition is dense, to sell products and services to consumers in the way as expected by the company has become harder but at the same time necessary compared to the past. It has become unavoidable for the firms to use various pricing strategies alongside with the classical selling strategies to reach this goal. In today’s economic conditions in which the markets being far from full competitive state resulted the firms functioning in this market to become more or less a price-maker. For this reason, one of the ways for the firms that aim to increase the total income thus the total profit can use is, to implement different pricing for consumers with different specialties instead of applying the same pricing for all the consumer groups. Because the consumers having different income levels, taste and choice cause them to have a desire to pay Continue reading

Correction of Balance of Payments (BoP) Deficit

Balance of Payments Adjustments The short-term and small deficits in balance of payments are quite likely to emerge in wide range of international transactions. These deficits do not call for immediate corrective actions. More importantly, irregular short-term changes in the domestic economic policies with a view to remove the short-term deficits in balance of payments may do more harms than good to the economy. Since these changes cause dislocations in the process of reallocation of resources and short-term fluctuations in the economy. Therefore, short-term deficits of smaller magnitude are not a serious concern to the policy makers. A constant deficit indicates that the country’s imports dominates exports or depreciation of its foreign exchange and gold reserves. These countries lose their international liquidity and credibility. This situation often leads to compromise with economic and political independence of these countries. India faced a similar situation in July 1990. Therefore, a country facing Continue reading

Law of Substitution or Equi-Marginal Utility – Definition, Significance and Criticisms

The law of substitution is also known as the law of equi-marginal utility or the law of maximum satisfaction. This law was first developed by H.H Gossen. Therefore, this law is also known as second law of Gossen. Prof. Marshall has developed and given the present shape of this law. This law states that in order to get maximum satisfaction, a consumer should spend his limited income on different commodities in such a way that the last dollar spent on each commodity yield him equal marginal utility. The law of substitution is also known as “The Law Of Maximum Satisfaction” because the consumer can maximize his/her satisfaction by spending income in accordance with this law. It is called “The Law Of Substitution” because the consumer will go on substituting one commodity with higher marginal utility for another commodity with lower marginal utility till the marginal utility of each commodity is Continue reading

Limitations of Break Even Analysis

To the management, the utility of break-even analysis lies in the fact that it presents a picture of the profit structure of a business firm. Break-even analysis not only highlights the areas of economic strength and weaknesses in the firm but also sharpens the focus on certain leverages which can be operated upon to enhance its profitability. Through break-even analysis, it is possible for the management to examine the profit structure of a business firm to the possible changes in business conditions. There are some important limitations of break-even analysis, which are to be kept in mind while using break-even analysis. These limitations are as follows: When break-even analysis is based on accounting data, it may suffer from various limitations, such as negligence towards imputed costs, arbitrary depreciation estimates and inappropriate allocation of overhead costs. Break-even analysis, therefore, can be sound and useful only if the firm in question maintains Continue reading