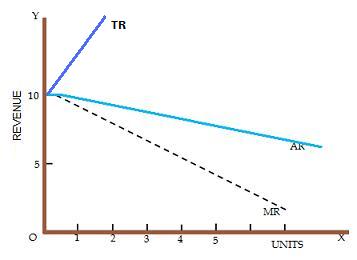

Monopoly is that market category in which a single seller dominates the market. There is only one producer (firm) and there are no substitutes for its product. Since under monopoly there is just one firm producing a particular product there is no element of competition. Besides in the absence of any other firm producing homogeneous product the firm itself constitutes the industry. Hence it is futile to make any effort to distinguish between a firm and an industry under monopoly. Under Monopoly, firm is itself an industry. The revenue structure under monopoly is bound to be different from that in case of a firm under perfect competition. Under perfect competition, the firm is a price-taker and not a price maker and its AR curve is horizontal denoted by perfectly elastic demand curve. But a monopolist is not a price-taker; he is price-maker. Continue reading

Economics Principles

The Principle of Equity in Taxation

Taxation traces its origin to the ancient times as a major source of revenue needed for governance. Kingdoms, monarchies and even dynasties had an elaborate form of taxation imposed on their subjects to source funds that were used to run affairs of the government. These taxes were subjective and biased depending on those in power. Advancement in education led to important studies on the possible forms of taxation that reflected the aspirations and welfare of the people. Owing to this therefore, Adam Smith, accredited as the “Father of modern political Economy” carried out an extensive study in Public Finance seeking to give an in-depth analysis of taxation. Smith documented the findings in his book known as “Wealth of Nations” in 1776. It is in this book that Smith scripted the four maxims of taxation which were later globally adopted as the Canons of Taxation which are summarized as Equity, Certainty, Continue reading

Why Oligopoly is a More Common Type of Market Structure Compared to Perfect Competition

Perfect competition is an ideal model and so it is difficult to find markets that have all these characteristics. There are some markets in the real world that approximates perfect competition. Examples of such markets are farming, the stock exchange market and the foreign currency market. These markets possess some of the characteristics of perfect competition as explained in part (a). However, even in such markets, some of the characteristics are hard to fulfil. For instance, buyers and sellers may not be price takers. In the stock exchange market, there are some individuals or institutions that can influence the price of shares through their large holdings of a particular company’s shares. The product is also not homogenous if stock of different companies are considered., Thus, if they were to sell their shares, price will fall. Knowledge is not perfect either. Although buyers and sellers do have easy access to information Continue reading

Types of Unemployment

The population of an economy is divided into two categories, the economically active and the economically inactive. The economically active population (labor force) or working population refers to the population that is willing and able to work, including those actively engaged in the production of goods and services (employed) and those who are unemployed. Whereas, unemployed refers to people who are willing and a capable of work but are unable to find suitable paid employment. The next category, the economically inactive population refers to people who are neither working nor looking for jobs. Examples include housewives, full time students, invalids,those below the legal age for work, old and retired persons. Unemployment is of different types. The important types of unemployment are: Structural unemployment: This is a type of unemployment caused mainly by the change in the development strategy adopted by an economy. For example, suppose a country basically agricultural in Continue reading

Cost Analysis of Multiple Products

Although, most modern firms make several products, Economic Theory has been developed on the premise that each firm produces only one product. The reasons for such inadequate premises are found partly in the historical origins of theory and partly in the simplicity of theoretical analysis when it is confined to production of just one single product. In many manufacturing enterprises two or more different products emerge from common production process and common raw-material used. Production of multiple product has almost become the rule. When two or more different products emerge from a single common production process and a single raw material, they get identified as separate products only at the end of common processing which is called the ‘Split of Point’. The costs that that have been incurred up-to the split of point are common costs. The common costs cannot be traced to the separate products. Some common costs are Continue reading

Pure Competition

In pure competition, the firm has to accept the given market price. At this given price, it can sell all the products, which it desires but at any higher price, it cannot sell anything. If the market price is below its cost, it has to either take the loss or withdraw from the market. As a result, any single firm in a purely competitive situation has to adjust its production and sales policies to the given market price. However, the market prices arc determined through the mutual consent of all the individual competitive buyers and sellers together. But any individual firm has no control over the price. Since a purely competitive seller has no control over the price at which he sells, his average marginal revenue schedule is infinitely elastic. In perfect competition, marginal revenue is equal to the average revenue, because every unit is sold at the same market Continue reading