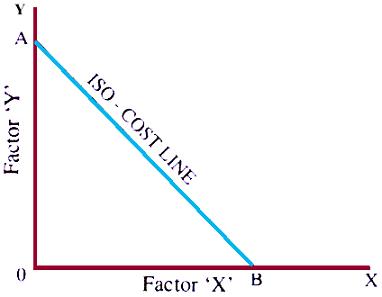

Given the Isoproduct map, the producer would like to ride on the highest possible Isoquant because any point on it would yield maximum possible output. But the producer’s desires are limited by his budgetary constraints. Before he selects a certain combination of inputs he has to take into consideration the size of his investment outlay and the prices of the factors of production. The Isocost Line Let us assume that the investment fund is given and the prices of factors X and Y are also known. On the basis of these assumptions let us suppose that the firm were to spend the entire amount on employing units of only input X. Then it could hireOB units of factor X. On the other hand if the producer wants to allocate his entire investment outlay in employing factor Y then he could hire OA units of Y. We have now obtained the Continue reading

Economics Principles

Different Types of Costs

Profit is the ultimate aim of any business and the long-run prosperity of a firm depends upon its ability to earn sustained profits. Profits are the difference between selling price and cost of production. In general the selling price is not within the control of a firm but many costs are under its control. The firm should therefore aim at controlling and minimizing cost. Since every business decision involves cost consideration, it is necessary to understand the meaning of various concepts for clear business thinking and application of right kind of costs. A managerial economist must have a clear understanding of the different cost concepts for clear business thinking and proper application. The several alternative bases of classifying cost and the relevance of each for different kinds of problems are to be studied. The various relevant concepts of cost are: Opportunity costs and Outlay costs: Out lay cost also known Continue reading

Pigovian Tax – Meaning and Definition

Neo-classicals uphold perfect competition as the ideal state of the market. But in truth, the economy is fraught with market failures. Therefore, we need government interference to correct many of these market failures. Pigovian Tax (also spelled Pigouvian tax) imposed by the government is one such course of intervention. It helps to curb negative externalities (e.g. pollution) and reduce the burden on the society caused by the externalities (social costs of production and consumption). Moreover, it attacks over-consumption, bringing it closer to the socially optimal level of production and/or consumption. What is Pigovian Tax? Pigovian tax is a kind of tax, which is levied to correct a negative cost that is created by the actions of any business firm, but that is not considered in a firm’s private costs or profits. Also known as ‘sin tax’, it is a tax placed on an action with a negative externality, to correct Continue reading

Principal-Agent Problem – Overview, Examples and Solutions

The significant discussion in business economics is principal-agent problems in organizations. A principal is a top authority who hires agents to act on his/her behalf, while an agent usually aims to achieve the objectives of the principal. A principal-agent problem arises when the activities of an agent impact on the principal’s interests. Although agents may seek to attain the goals set by principals but may sometimes fail to carry out those targets. The conflict between shareholders (as principals) and managers (as agents) is a good example of principal-agent problem. When ownership and control is divided between the principals and agents in an organisations this gives the agents opportunity to pursue the goals that may not agree with the desires of the principals. A lot of principal-agent relationships may be found in human society such as patients and doctors, shareholders and managers, managers and workers. But shareholder-manager and manager-workers are the Continue reading

Cost Control Concepts

The long-run prosperity of a firm depends upon its ability to earn sustained profits. Profit depends upon the difference between the selling price and the cost of production. Very often, the selling price is not within the control of a firm but many costs are under its control. The firm should therefore aim at doing whatever is done at the minimum cost. In fact, cost control is an essential element for the successful operation of a business. Cost control by management means a search for better and more economical ways of completing each operation. In effect, cost control would mean a reduction in the percentage of costs and, in turn, an increase in the percentage of profits. Naturally, cost control is and will continue to be of perpetual concern to the industry. Cost control has two aspects such as a reduction in specific expenses and a more efficient use of Continue reading

Keynesian Theory and Underdeveloped Countries

Lord John Maynard Keynes wrote the General Theory of Employment, Interest and Money as a solution to the problem of periodic unemployment faced by developed industrial nations of the West during the great depression of the thirties. Keynesian theory singles out deficiency of effective demand as the major cause of unemployment and low level of income in industrial economy operations under a laissez faire system. Deficiency of effective demand is a prominent feature of economies undergoing depression and in order to improve the level of effective demand in an economy. Keynes suggested policy measures like cheap money policy, government’s compensatory investment spending, deficit financing and other fiscal methods. In essence, therefore, Keynesian economics turn out to be economics of depression applicable to developed countries. Its applicability in underdeveloped countries is very limited. To quote Joan Robinson: “ Keynes’s theory has little to say directly, to the underdeveloped countries, for Continue reading