In a market economy, commerce and customers make a decision of their own decision what they will consume and manufacture, and in which conclusions on the allotment of those sources are without government interference. Hypothetically this denotes that the manufacturer is required to decide what to produce, how much to produce, what prices to set up for consumers for those productions, what to pay workers, and so on. These conclusions in a market financial system are impacted by the forces of competition, supply, and demand. This is frequently distinguished with a premeditated economy, where central government concludes what will be manufactured and in what amounts. A market economy is also compared with the mixed economy where there are market processes through the system of markets that is not completely free but under some state control that is not widespread enough to comprise a deliberate financial system. In reality, there is Continue reading

Economics Principles

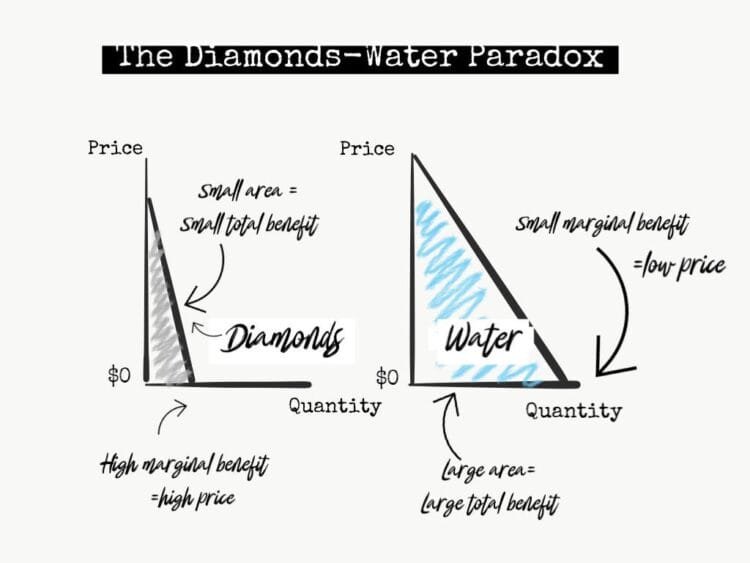

The Diamond-Water Paradox in Economics

The concept of the value of goods was one of the most actively discussed topics by economists in the 18-19th century. In “A Study of the Nature and Causes of the Wealth of Nations,” published in 1776, Adam Smith voiced the question that would later become known as the diamond-water paradox. It sounded like this: “There is nothing more useful than water: but you can hardly buy anything with it… Diamond, on the contrary, has almost no use-value; but a very large number of other goods can often be obtained in exchange for it”. The classical economists Adam Smith and Karl Marx considered a product’s value concerning how it satisfies a human need. The price was associated with the effort and labor expended to meet a specific demand. Besides, classical economists used the concepts of use-value and exchange-value, which determine the nature and exchange value of products. Later, in the Continue reading

Econometric Forecasting Models

Econometric model building holds considerable promise as a method of forecasting demand. The best starting point towards an understanding of the basis of econometric forecasting is regression analysis. But the difficulty with regression analysis is that it is used to forecast a single dependent variable based on the value and the relations between one or more independent variables and each of these independent variables is assumed to be exogenous or outside the influence of the dependent variable. This may be true in many situations. But unfortunately, in most broad economic situations an assumption that each of the variable, is independent is unrealistic. For example, let us assume that demand is a function of Gross National Product (GNP), price and advertising. In regression terms we would assume that all three independent variables are exogenous to the system and hence are not influenced by the level of demand itself or by one Continue reading

Government – Meaning and Roles

Government is one of humanity’s oldest and most important institutions. Since the early times, some kind of government has been an important source in the society. Every society needs some people to make and enforce decisions upon the society and the government refers to the process of exercising power in a group. Government generally means the public government as of a nation, state, province, country, city or village. Government affects the activity of every human in important ways. Form of government refers to the set of political institutions by which a government of a state or a country is organized. Each successive government is composed of a body of individuals who control and exercises control over political decision-making. Their function is to make and enforce laws and arbitrate conflicts. In some countries and states this group is often of hereditary class and in some of democracy, where political roles remain Continue reading

Usage of Macroeconomics for Business Decisions

Decision making is an important job of corporate managers. They have to take decisions regarding the employment of land, labor, and capital in such a manner that output may be maximized at least possible cost. Hence, they are always in search of optimum combination of resources which would maximize corporate profit. Appropriate decision making is the strength of business. Success in business depends on proper and correct decision making. Location, scale of operation, quantum of resources to be employed, marketing etc are some of the important problems calling for decisions in business where macroeconomics may be applied for better results. Macro Economic Analysis Macroeconomics is concerned with the study of aggregate economic variables. It is concerned with the whole economy and studies the level and the growth of national income, the levels of employment, the level of private and government spending, the balance of payments, the consumption & the investment, saving functions Continue reading

Price Analysis and Theory of the Firm

To understand the concept of market and its various conditions, it is necessary to study the theory of the firm. This is discussed as follows: The basic, assumptions of the theory of the firm are as follows: The objective of a firm is to maximize net revenue in the face of given prices and technologically determined production function. A price increase far a product raises its supply, whereas prices increase for a factor reduces its demand. The theory of the firm deals with the role of business firms in the resource allocation process. It uses aggregation as a tactic and attempts to specify total market supply and demand curves. The firm operates with perfect knowledge of all relevant variable involved in making a decision and it acts rationally while doing so. Originally the theory assumed that the firm is operating within a perfectly competitive market. But it has now been Continue reading