The major sales tax provisions relevant for leasing are as follows: The lessor is not entitled for the concessional rate of central sales tax because the asset purchased for leasing is meant neither for resale nor for use in manufacture. (It may be noted that if a firm buys an asset for resale or for use in manufacture it is entitled for the confessional rate of sales tax). The 46th Amendment Act has brought lease transitions under the purview of ‘sale’ and has empowered the central and state government to levy sales tax on lease transactions. While the Central Sales Tax Act has yet to be amended in this respect, several state governments have amended their sales tax laws to impose sales tax on lease transactions. a. Levy of Sales Tax: Sales Tax is leviable when goods are sold. Thus there must be ” Goods and there must be a Continue reading

Financial Services

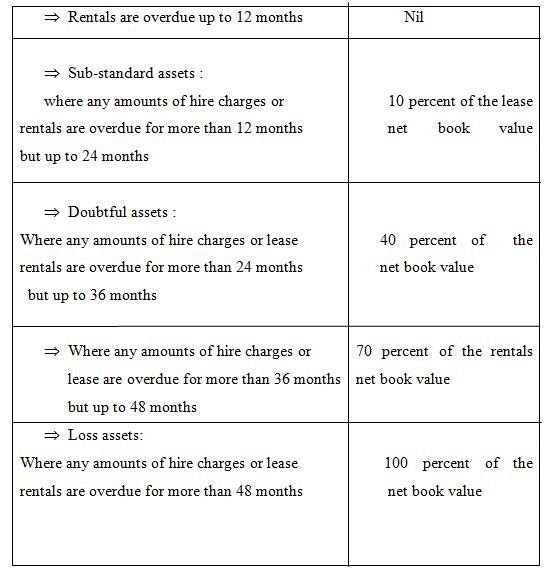

Accounting Treatments for Non-Performing Leases

There is no information in the guidance note on lease accounting, 1995, for non-performing assets. The general accounting principles for non-performing assets is contained in accounting standard 9 on Revenue Recognition which is more or less on the lines of the International Accounting Standards on the issue. The Standard provides that whereas, in general, incomes are to be recognized on the basis of accrual, in case of an uncertainty in the ultimate realization of an income, the treatment is as follows: If the uncertainty is prevalent at the time of raising the claim for the income, the recognition of the income shall be postponed If the uncertainty arises subsequent to the claim being made, there shall be a provision made to the extent of the uncertainty. This statement lays down the basic difference between a provision against an income, and non-recognition of income, which is very significant. The accounting for Continue reading

Principal Functions of Investment Banks

Global investment banks typically have several business units, each looking after one of the functions of investment banks. For example, Corporate Finance, concerned with advising on the finances of corporations, including mergers, acquisitions and divestitures; Research, concerned with investigating, valuing, and making recommendations to clients – both individual investors and larger entities such as hedge funds and mutual funds regarding shares and corporate and government bonds; and Sales and Trading, concerned with buying and selling shares both on behalf of the bank’s clients and also for the bank itself. For Investment banks management of the bank’s own capital, or Proprietary Trading, is often one of the biggest sources of profit. For example, the banks may arbitrage stock on a large scale if they see a suitable profit opportunity or they may structure their books so that they profit from a fall in bond price or yields. In short the principal Continue reading

Problems of Leasing

Leasing has great potential in India. However, leasing in India faces serious handicaps which may mar its growth in future. The following are some of the problems. 1. Unhealthy Competition: The market for leasing has not grown with the same pace as the number of lessors. As a result, there is over supply of lessors leading to competitor. With the leasing business becoming more competitive, the margin of profit for lessors has dropped from four to five percent to the present 2.5 to 3 percent. Bank subsidiaries and financial institutions have the competitive edge over the private sector concerns because of cheap source of finance. 2. Lack of Qualified Personnel: Leasing requires qualified and experienced people at the helm of its affairs. Leasing is a specialized business and persons constituting its top management should have expertise in accounting, finance, legal and decision areas. In India, the concept of leasing business Continue reading

Some Variants of Leases

1. Direct Lease A direct lease can be defined as any lease transaction which is not a “sale and leaseback” transaction. In other words, in a direct lease, the lessee and the owner are two different entities. A direct lease can be of two types: Bipartite Lease and Tripartite Lease. Bipartite Lease In a bipartite lease, there are two parties to the transaction – the equipment supplier cum-lessor and the lessee. The bipartite lease is typically structured as an operating lease with in-built facilities like up gradation of the equipment (upgrade lease) or additions to the original equipment configuration. The lessor undertakes to maintain the equipment and even replaces the equipment that is in need of major repair with similar equipment in working condition (swap lease). Of course, all these add-ons to the basic lease arrangement are possible only if the lessor happens to be a manufacturer or a dealer Continue reading

Merchant Banking Services: Management of Capital Issues

The capital issue are managed are category-1 merchant banker and constitutes the most important aspects of their services. The public issue of corporate securities involves marketing of capital issues of new and existing companies, additional issues of existing companies including rights issue and dilution of shares by letter of offer. The public issues are managed by the involvement of various agencies i.e. underwriters, brokers, bankers, advertising agency, printers, auditors, legal advisers, registrar to the issue and merchant bankers providing specialized services to make the issue of the success. However merchant banker is the agency at the apex level than that plan, coordinate and control the entire issue activity and direct different agencies to contribute to the successful marketing of securities. The procedure of the managing a public issue by a merchant banker is divided into two phases, viz; Pre-issue management Post-issue management Pre-Issue Management: Steps required to be taken to Continue reading