Traditional macroeconomic exchange-rate models are based on fundamental analyses. In these models, the basic force that drives currency’s rate comes from the balance between supply and demand of currency, for example if the demand for the U.S. dollar exceeds its supply at the current exchange-rate against the euro the price of US dollar in terms of the euro will rise. Conversely, if supply exceeds demand, the price will fall. Demand and supply factors that govern currency’s rate’s become much more complex than that because people don’t use currencies just to purchase foreign goods and services, but also for activities like cross-border investment and speculation. This opens up many other variables that must be considered when addressing exchange-rate movements, as underscored in the Federal Reserve Bank of New York’s commentary cited previously. One of the most important factors, for example, is how investors ride interest-rate differentials between countries. We know that Continue reading

Forex Investments

Fixed and Option Forward Contracts and it’s computation

Under the fixed forward contract the delivery of foreign exchange should take place on a specified future date. Then it is known as ‘fixed forward contract’. Suppose a customer enters into a three months forward contract on 5th January with his bank to sell Euro 15,000, then the customer would be presenting a bill or any other instrument on 7th April to the bank for Euro 15,000. The delivery of foreign exchange cannot take place prior to or later than the determined date. Though forward exchange is a mechanism wherein the customer tries to over come the exchange risk, the purpose will be defeated if the delivery of foreign exchange does not take place exactly on the due date. Practically speaking, it is not possible for any exporter to determine in advance the precise date on which he will be tendering export documents for reasons which are internal relating to Continue reading

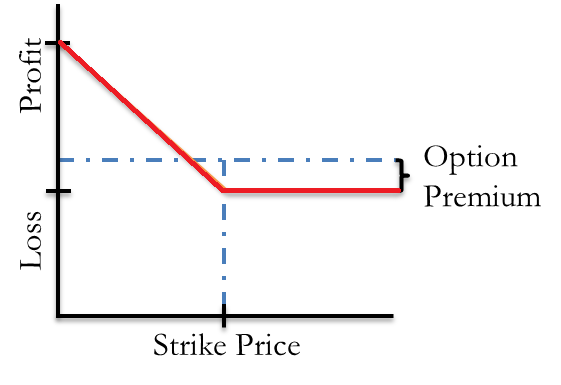

Put Option

An option is a contract, which gives the buyer the right to buy or sell foreign currency at a specific price, on or before a specific date. For this, the buyer has to pay to the seller some money, which is called as premium. There is no obligation on the buyer to complete the transaction if the price is not favorable to him. Whenever a person has an intention to sell foreign currency by paying a premium amount immediately and settling the same on a later date, it is known as a Put Option. Put Option has two parties, one a buyer of a Put Option and other a seller of a Put Option. Example: Mr. A is interested in selling a US Dollar. Spot rate is US$ 1 = 45.50. Mr. A believes that some 15 days down the line, with the budget coming up, the price of the Continue reading

Economic Exposure of Foreign Exchange Risk

Economic exposure is concerned with the present value of future operating cash flows to be generated by a company’s activities and how this present value, expressed in parent currency, changes following the foreign exchange rate movements. The concept of economic exposure of foreign exchange risk is most frequently applied to a company’s expected operating cash flows from foreign operations, but it can equally well be applied to a firm’s home territory operations and the extent to which the present value of those operations alters resultant upon changed exchange rates. For the purpose of convenience, the exposition that follows is based on a firm’s foreign operations. Some experts classify transaction exposure as a subset of economic exposure. They take this view arguing that the present value of an uncovered foreign currency denominated receivable or payable will vary as exchange rates vary. Whilst we accept the logic of this view, in this Continue reading

Management of Foreign Exchange Risks

What gives rise to foreign exchange transactions? Basically, there are four important factors which give rise to foreign exchange deals or transactions: (a) trade (exports/imports); (b) transfer (remittances); (c) investment (say, FCNR transactions); and (d) speculation. If one were to ask what is the proportion of speculation to the first three in the global foreign exchange market, one would be shocked to know that speculation accounts for nearly 96 per cent of the foreign exchange turnover of about US$ 700 billion per day in the international foreign exchange market. As we are aware, banks have established huge dealing rooms, and foreign exchange dealers are consistently buying and selling foreign currencies to make profits for their own institutions. Although speculation or pure dealing, as opposed to a merchant transaction, is anathema to banking, it is not “uncontrolled” speculation, as most senior managements of banks have imposed stringent controls to contain exposures Continue reading

Understanding the Financial Swaps Market

Exchange rate instability and the collapse of the Bretton Woods System and particularly the control over the movement of the capital internationally, paved the way for the origin of the financial swaps market. To day swaps are at the center of the global financial revolution. The growth is such that sometimes it looks like unbelievable but it is true. Though its growth will continue or not is doubtful. Already the shaking has started. In the “plain vanilla” dollar sector, the profits for brokers and market makers, after costs and allocation of risk capital, are measured in fewer than five basis points. This is before the regulators catch up and force disclosure and capital haircuts. At these spreads, the more highly paid must move on to currency swaps, tax-driven deals, tailored structures and schlock swaps. The fact which is certain is that, although the excitement may diminish, swaps will stay. Already, Continue reading