Relationship Between Organizational Behavior and Management Control System

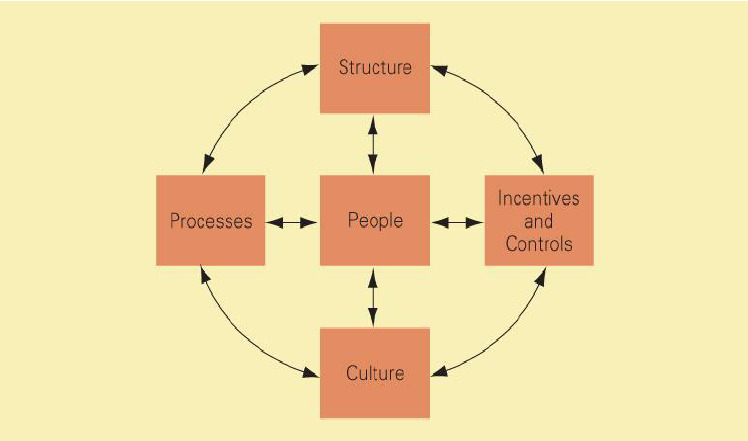

Organizational Behavior and Management Control There is a close relationship between organizational behavior and management control system. A management control system seek to evaluate and regulate the performance of responsibility centers. The manager in charge of a responsible center is rewarded for good performance. At the same time when the performance of a responsibility center is dismal, the manager in charge is punished. Thus, a management control system acts as a double-edged sword. That is why manager are afraid of a control system and, may resist it. In order to make a control system successful, it is necessary to understand the factors that motivate, managers to achieve the results. Behavioral sciences have given several concepts that are relevant to management control. Some of these concepts at described below. 1. Perception. Whether a management control system is accepted and implemented successfully does not depend on the system. It depends largely on Continue reading