Olympus is a Japanese company that specializes in medical imaging tools and photo/video cameras. Back in the 1980s, when the operating income of the company decreased due to the sharp appreciation of the yen, the Olympus executives started an aggressive financial assets management in order to shift losses off the company’s balance sheet. As a result, Olympus has managed to hide $1.7 billion of investment losses for more than a decade. The case of Olympus is the example of the financial statement fraud in which an employee intentionally causes a misstatement or omission of material information in the organization’s financial reports that eventually results in median loss of $1 million. To conceal the losses, the company has developed a tobashi scheme in which they booked the company’s assets at historical cost instead of fair market value. In 1997, the Japanese legislation was reformed, and since then all the assets should Continue reading

Financial Scams

Case Study: The Story Behind the Olympus Scandal

In the 1980s, several Japanese corporations experienced financial challenges as they depended on investments to boost their declining profits. One of the main reasons was that the country’s export had been damaged by the strength of its currency against other currencies, especially the US Dollar. Olympus became one of the number one victims of Japan’s economic situation. Because the company was struggling with its business operations, it decided to use a Japanese concept known as zaitech, which refers to financial engineering in salvaging the situation. Consequently, the company decided to invest in risky businesses and financial derivatives in order to boost its profits. Nevertheless, the business ventures caused huge losses of about 2.1 billion Yen in the early 1990s. It is during that time when the management of the Olympus devised ways of concealing the huge losses from the published financial reports. Although it has been able to hide the Continue reading

Case Study on Business Ethics: Accounting Fraud at Nortel Networks Corporation

For more than 10 decades, Nortel is engaged in the supply of telecommunications equipment for Canada’s telephone systems. In the 1890s, the company started manufacturing manually, operated switchboards, which have later turned into establishing the fiber-optic systems for the Internet today. Nortel Networks Corporation is having its headquarters in Brampton, Ontario, Canada was considered as one of the leaders of the telecommunications industry during the late 1990s. About three-fourths of the Internet traffic of North America was transacted through Nortel equipment. Nortel had around 73,000 employees around the world. The company’s share was listed on both at the “Stock Exchanges” of Canada and New York. Nortel had a market capitalization at a peak price of C$ 124.5O and had over 3.8 billion shares worth C$473.1 billion as of July 2000. Nortel accounted for over thirty percent of the value of the S & P / TSE 300 Composite index. Nortel has been Continue reading

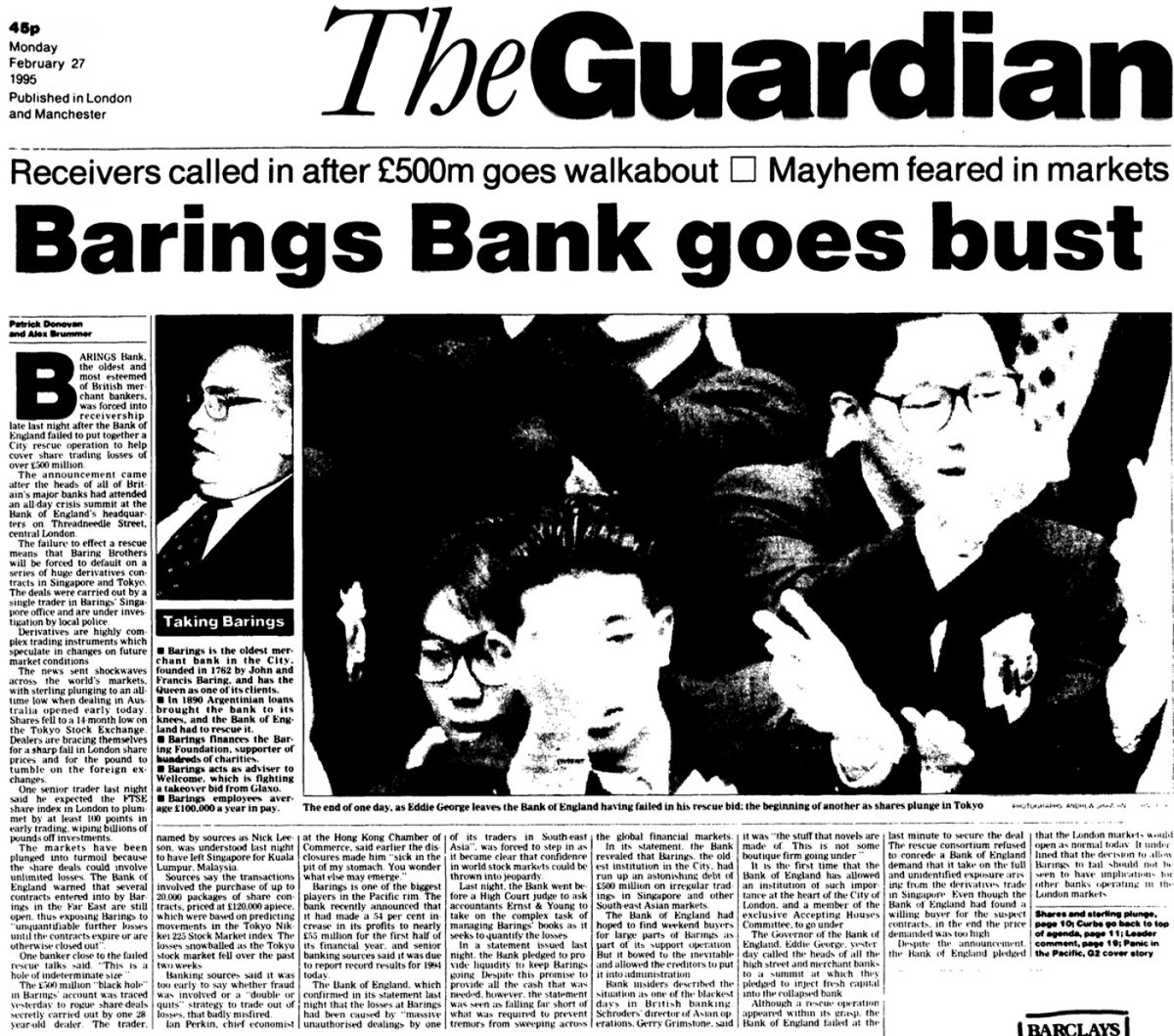

Case Study: Nick Leeson and the Collapse of Barings Bank

In 1985, Nick Leeson had a job as a clerical work at Coutts & Co. The Coutts & Co is a private banking house in United Kingdom which own by aristocrat. This bank was a subsidiary of the National Westminster Bank. During that period, the stock markets were rising for several years and the bank were expanding into a new financial instruments coming in and demand for labor was high. During that time, Nick Leeson was the person who had many working class young men. After two years, Nick Leeson moved to Morgan Stanley, one of the US investment bank. Nick Leeson be a settlements clerk at that bank. Nick Leeson can absorb more knowledge about new derivatives market from that bank. In 1989, Nick Leeson was applying a for job at Baring Securities due to his own knowledge with trading in Japan, that time Nick Leeson was 22 years Continue reading

Case Study on Corporate Governance: WorldCom Scandal

Established in 1988, WorldCom was formed so that the strongest, most capable public relations firms could serve national and international clients, while retaining flexibility and client- service focus inherent in independent agencies. Through WorldCom, clients have on demand access to in-depth communication expertise from professionals who understand the language, culture and customs in the geographic areas of operation. WorldCom has 105 offices in 90 cities and 40 countries on five continents, more than 2000 employees and recorded revenue of US $ 243.5 million in 2008. In the 90’s WorldCom was involved in acquisitions and purchased over 60 firms. The complete financial integration of the acquired company must be accomplished, including an accounting of assets, debts, and a host of other financially important factors. WorldCom moved into Internet Traffic, controlling 50% of US Internet Traffic and 50% of the e-mails worldwide. In 1997, WorldCom and MCI completed a US $37 billion Continue reading

Ethics in Financial Reporting

Integrity is of utmost importance for a successful career in business and finance in the long run. Some believe that the world of finance lacks ethical considerations. Whereas the truth is that such issues are prevalent in all areas of business. The business environment in much of the world is reeling from the revelation of several financial scandals in the past few years. The optimism of the turn of the century has been replaced by scepticism and distrust. It will be discussed as to how we landed ourselves in this situation, what is being done to correct it, and what the future holds for us. Though Enron has been used as the poster-child for this purpose, breakdowns in accounting and corporate governance in Enron as well as in other companies will be discussed. Some companies that have encountered financial reporting problems will be discussed along with the role of auditors Continue reading