Modern Portfolio Theory – Markowitz Portfolio Selection Model

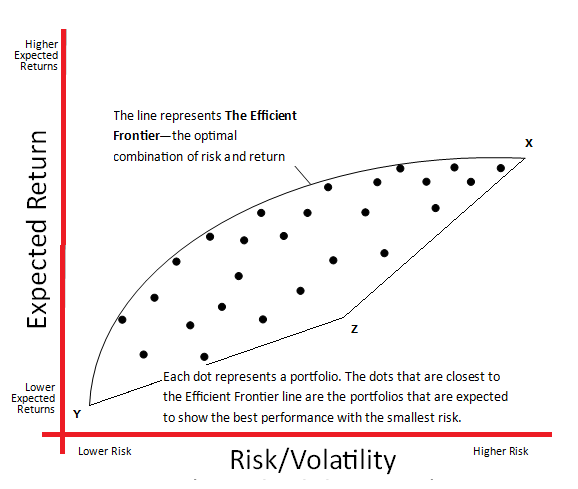

Markowitz Portfolio Theory Harry Markowitz developed a theory, also known as Modern Portfolio Theory (MPT) according to which we can balance our investment by combining different securities, illustrating how well selected shares portfolio can result in maximum profit with minimum risk. He proved that investors who take a higher risk can also achieve higher profit. The central measure of success or failure is the relative portfolio gain, i.e. gain compared to the selected benchmark. Modern portfolio theory is based on three assumptions about the behavior of investors who: wish to maximize their utility function and who are risk averse, choose their portfolio based on the mean value and return variance, have a single-period time horizon. Markowitz portfolio theory is based on several very important assumptions. Under these assumptions a portfolio is considered to be efficient if no other portfolio offers a higher expected return with the same or lower risk. Continue reading