Portfolio management is a process encompassing many activities of investment in assets and securities. It is a dynamic and flexible concept and involves regular and systematic analysis, judgment and action. The objective of this service is to help the unknown and investors with the expertise of professionals in investment portfolio management. It involves construction of a portfolio based upon the investor’s objectives, constraints, preferences for risk and returns and tax liability. The portfolio is reviewed and adjusted from time to time in tune with the market conditions. The evaluation of portfolio is to be done in terms of targets set for risk and returns. The changes in the portfolio are to be effected to meet the changing condition. Portfolio construction refers to the allocation of surplus funds in hand among a variety of financial assets open for investment. Portfolio theory concerns itself with the principles governing such allocation. The modern Continue reading

Portfolio Management

Need of Good Investment Decisions

Investments are both important and useful in the context of present day conditions. The following points have made investment decision increasingly important. Planning for retirement Interest rate High rate of inflation Increase rate of taxation Income Investment channels 1. Planning for retirement: A tremendous increase in working population, proper plans for life span and longevity have ensured the need for investment decisions. Investment decision have becomes significant as working people retire between the age 55 and 60. The life expectancy has increased due to improved living conditions, medical facilities etc. The earnings from employment should, therefore, be calculated in such a manner that a portion should be put away as savings. Saving from the from the current earning must be invested in a proper way so that principal and income thereon will be adequate to meet expenditure on them after their retirement. 2. Interest rate: The level of interest rates Continue reading

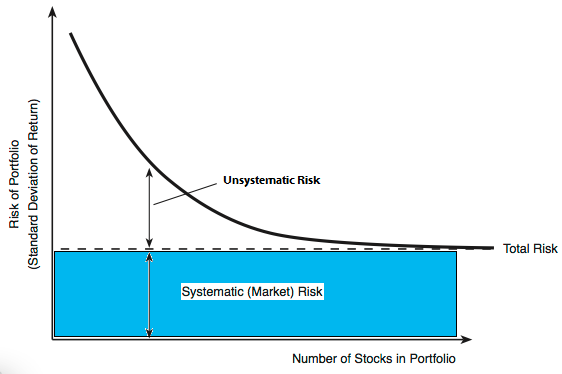

Portfolio Diversification with a Number of Securities

The benefits from diversification increase, as more and more securities with less than perfectly positively correlated returns are included in the portfolio. As the number of securities added to a portfolio increases, the standard deviation of the portfolio becomes smaller and smaller. Hence an investor can make the portfolio risk arbitrarily small by including a large number of securities with negative or zero correlation in the portfolio. But in reality, no securities show negative or even zero correlation. Typically, securities show some positive correlation, which is above zero but less than the perfectly positive value (+1). As a result, diversification (that is, adding securities to a portfolio) results in some reduction in total portfolio risk but not in complete elimination of risk. Moreover, the effects of diversification are exhausted fairly rapidly. That is, most of the reduction in portfolio standard deviation occurs by the time the portfolio size increases to Continue reading

Risk and Return in Portfolio Investments

Risk in Portfolio Investments The Webster’s New Collegiate Dictionary definition of risk includes the following meanings: “……. Possibility of loss or injury ….. the degree or probability of such loss”. This conforms to the connotations put on the term by most investors. Professional often speaks of “downside risk” and “upside potential”. The idea is straightforward enough: Risk has to do with bad outcomes, potential with good ones. In considering economic and political factors, investors commonly identify five kinds of hazards to which their investments are exposed. The following are different components of risks associated with portfolio investments: A. Systematic Risk Systematic risk refers to the portion of total variability in return caused by factors affecting the prices of all securities. Economic, Political and Sociological changes are sources of systematic risk. Their effect is to cause prices of nearly all individual common stocks or security to move together in the same Continue reading

Arbitrage Pricing Theory (APT) – Definition and Formula

A substitute and concurrent theory to the Capital Asset Pricing Model (CAPM) is one that incorporates multiple factors in explaining the movement of asset prices. The arbitrage pricing model (APT) on the other hand approaches pricing from a different aspect. It is rarely successful to analyze portfolio risks by assessing the weighted sum of its components. Equity portfolios are far more diverse and enormously large for separate component assessment, and the correlation existing between the elements would make a calculation as such untrue. Rather, the portfolio’s risk should be viewed as a single product’s innate risk. The APT represents portfolio risk by a factor model that is linear, where returns are a sum of risk factor returns. Factors may range from macroeconomic to fundamental market indices weighted by sensitivities to changes in each factor. These sensitivities are called factor-specific beta coefficients or more commonly, Continue reading

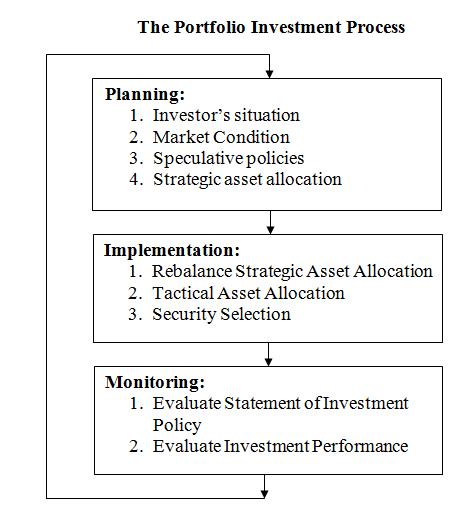

Portfolio Investment Process

The ultimate aim of the portfolio manager is to reduce the risk and increase the return to the investor in order to reach the investment objectives of an investor. The manager must be aware of the portfolio investment process. The process of portfolio management involves many logical steps like portfolio planning, portfolio implementation and monitoring. The portfolio investment process applies to different situation. Portfolio is owned by different individuals and organizations with different requirements. Investors should buy when prices are very low and sell when prices rise to levels higher that their normal fluctuation. Portfolio Investment Process Portfolio investment process is an important step to meet the needs and convenience of investors. The portfolio investment process involves the following steps: Planning of portfolio. Implementation of portfolio plan. Monitoring the performance of portfolio. 1. Planning of Portfolio Planning is the most important element in a proper portfolio management. The success of Continue reading