Advantages of Market-Neutral Alternative Funds One of the vital advantages characteristic of market-neutral alternative funds is the lowest correlation rate compared to other assets. Even though the return pattern would change for the organization over time, it would still have the opportunity to mitigate risks by combining different strategies based on market-neutral alternative funds. Investment options are not being seen as the essential way of creating a fortune in this case because investors do not associate themselves with fortunes. This is usually done to reduce the impact of the broader market on the organization and create a cushion for the company that would protect the lower levels of correlation from increasing drastically. Overall, market-neutral alternative funds are advantageous for correlation rates because they broaden the list of asset classes that are eligible for improvement. A decreased level of volatility is another benefit typical of market-neutral alternative funds. Investment lineups of Continue reading

Stock Investments

Option Trading in Shares and Currency Options

Option Trading in Shares and Stocks When an option contract is entered into with an option to buy or sell shares or stocks, it is known as ‘share option’. Share option transactions are generally index-based. All calculations are based on the change in index value. For example, the present value of the index is Rs.300 and the strike price or exercise price is Rs.350. So long as the index remains below 350, the option holder will not exercise his option since he will be incurring losses. Now, the loss will be limited to the premium paid at the rate of Rs. 10/- per point. As the spot price increases beyond the strike price level, exercise of the option becomes profitable. Suppose the spot rate reaches 360, option may be exercised. The option holder gets a profit of Rs. 100 (10 points x 10). However, his net position will be Rs. Continue reading

Features of Option Contract

Some important features of Options Contract are: 1. Highly flexible: On one hand, option contract are highly standardized and so they can be traded only in organized exchanges. Such option instruments cannot be made flexible according to the requirements of the writer as well as the user. On the other hand, there are also privately arranged options which can be traded ‘over the counter’. These instruments can be made according to the requirements of the writer and user. Thus, it combines the features of ‘futures’ as well as ‘forward’ contracts. 2. Down Payment: The option holder must pay a certain amount called ‘premium’ for holding the right of exercising the option. This is considered to be the consideration for the contract. If the option holder does not exercise his option, he has to forego this premium. Otherwise, this premium will be deducted from the total payoff in calculating the net Continue reading

Understanding the Financial Swaps Market

Exchange rate instability and the collapse of the Bretton Woods System and particularly the control over the movement of the capital internationally, paved the way for the origin of the financial swaps market. To day swaps are at the center of the global financial revolution. The growth is such that sometimes it looks like unbelievable but it is true. Though its growth will continue or not is doubtful. Already the shaking has started. In the “plain vanilla” dollar sector, the profits for brokers and market makers, after costs and allocation of risk capital, are measured in fewer than five basis points. This is before the regulators catch up and force disclosure and capital haircuts. At these spreads, the more highly paid must move on to currency swaps, tax-driven deals, tailored structures and schlock swaps. The fact which is certain is that, although the excitement may diminish, swaps will stay. Already, Continue reading

Bonus Issue of Shares – Meaning, Benefits and Motives

BONUS ISSUE OF SHARES When we invest the share capital in a business, we do so with the expectation of getting back not only our invested capital, but also a proportionate share of the surplus generated from operations, after all the other stakeholders have been paid their dues. Thus, collectively the business owes its shareholders, their invested capital as well as the surplus generated from operations. But in reality, while the business may pay us annual dividends, seldom is this surplus fully distributed away as dividends. Thus, the surplus which is retained in the business is still owed to us. This retained surplus is also reflected as retained earnings or reserves in the Balance sheet of a company. Together, share capital and reserves are known as equity or the net worth of a company. Over a period of time, the retained earnings of a firm Continue reading

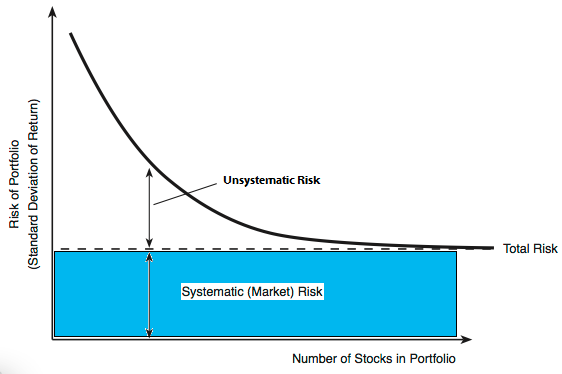

Portfolio Diversification with a Number of Securities

The benefits from diversification increase, as more and more securities with less than perfectly positively correlated returns are included in the portfolio. As the number of securities added to a portfolio increases, the standard deviation of the portfolio becomes smaller and smaller. Hence an investor can make the portfolio risk arbitrarily small by including a large number of securities with negative or zero correlation in the portfolio. But in reality, no securities show negative or even zero correlation. Typically, securities show some positive correlation, which is above zero but less than the perfectly positive value (+1). As a result, diversification (that is, adding securities to a portfolio) results in some reduction in total portfolio risk but not in complete elimination of risk. Moreover, the effects of diversification are exhausted fairly rapidly. That is, most of the reduction in portfolio standard deviation occurs by the time the portfolio size increases to Continue reading