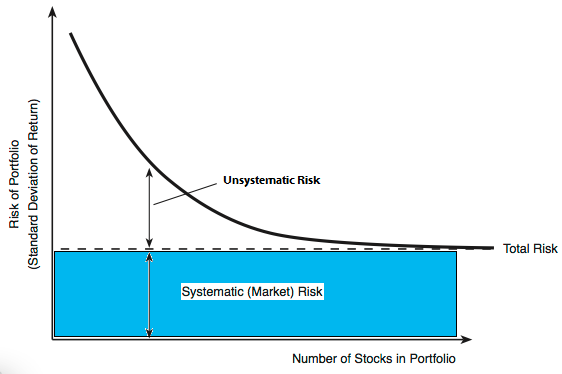

Portfolio Diversification with a Number of Securities

The benefits from diversification increase, as more and more securities with less than perfectly positively correlated returns are included in the portfolio. As the number of securities added to a portfolio increases, the standard deviation of the portfolio becomes smaller and smaller. Hence an investor can make the portfolio risk arbitrarily small by including a large number of securities with negative or zero correlation in the portfolio. But in reality, no securities show negative or even zero correlation. Typically, securities show some positive correlation, which is above zero but less than the perfectly positive value (+1). As a result, diversification (that is, adding securities to a portfolio) results in some reduction in total portfolio risk but not in complete elimination of risk. Moreover, the effects of diversification are exhausted fairly rapidly. That is, most of the reduction in portfolio standard deviation occurs by the time the portfolio size increases to Continue reading